The basics of retiring with DRS

Once you’ve reached the required age and years of service for your plan, you can apply for your pension retirement through DRS. We have a complete retirement checklist as well as live and recorded seminars to guide you through the retirement process, but basically it goes like this:

1. Make sure you qualify for retirement. Do you meet the age requirements? Do you have the number of service years needed for your plan? See your plan page for age and service requirements. This is also a great time to run a quick estimate of the retirement income you’ll receive by using the benefit estimator tool in your online account.

2. Request an official benefit estimate from DRS 3 to 12 months prior to your retirement date. Make this request through your online account or by contacting us. In most cases, we will provide your estimate 5 to 8 weeks before your retirement date. If you haven’t received your requested estimate within 5 weeks of your retirement date, contact us.

Estimates are prioritized by retirement date, which allows DRS to use the most recent information available for you and gives you ample time to submit your retirement application. An official benefit estimate is not the same as the benefit estimator tool available to all customers. However, the dollar amounts you preview in both estimates will likely be similar. Use the benefit estimator tool through your online account to assist your retirement planning any time before or after requesting your official benefit.

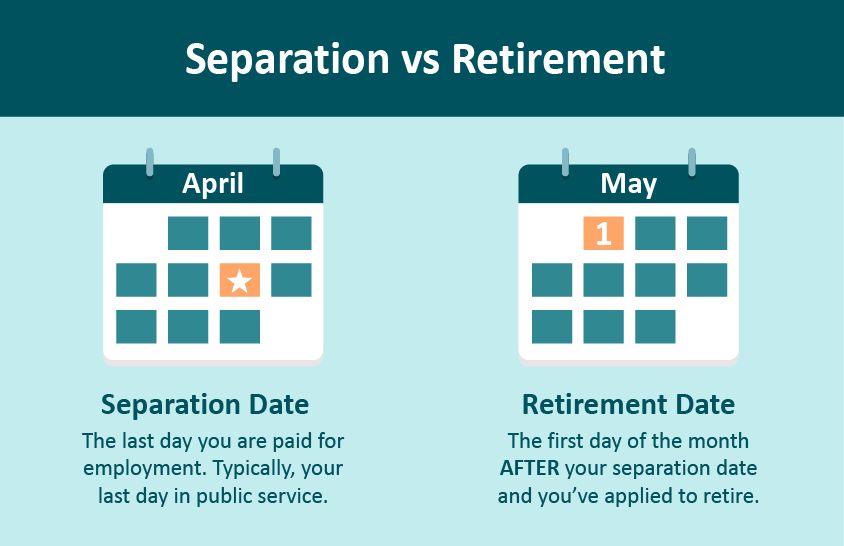

3. Complete a retirement application We recommend you apply at least 3-5 weeks from the date you intend to retire (once you receive your official estimate). If you can’t make this timeline, contact us right away so we can help keep your retirement on track. Complete the application online or request a paper form. For a preview of the questions you’ll answer while retiring, as well as a checklist of information to gather, see this example retirement application.

At any point in your retirement journey, you are welcome to attend a free nearing retirement seminar, hosted by DRS. The following video offers a preview of the online DRS retirement application:

Are you in more than one plan?

If you are a member of more than one Washington state retirement system, you are a dual member. You can combine service credit earned in all dual member systems to become eligible for retirement. However, being a dual member does require more attention than a single-plan retirement. For example, you’ll need to apply for your pension using a paper retirement application. Visit this section for members of multiple plans to find out more.

Consider your DCP income

If you have a DCP account, you can access these funds separately anytime after you leave employment. You can complete this withdrawal online or contact the DRS record keeper, Voya Financial at 888-327-5596. See DCP withdrawals for more.

If your employer offers DCP, and provides compensation for unused leave, consider deferring these cash-outs into DCP to maximize your savings at retirement. Find out more about leave deferrals.

Plan 3 has two separate parts

If you are in Plan 3 you have two sources of retirement income:

- The investment account you contribute to throughout your career.

- Your employer-funded pension account.

Plan 3 members access these income sources separately.

This means you will submit two separate requests for collecting the funds in retirement. You’ll have your pension retirement application you complete with DRS (step 3 above), and you’ll set up withdrawal for your investment funds. Access your investment funds through the DRS record keeper, Voya Financial.

Here’s the convenience of having two parts to your Plan 3 account – You don’t have to collect this retirement income at the same time. You can choose to postpone receiving either. When you reach age 73, the IRS requires you to begin withdrawing funds from your investment account—otherwise, the timeline is up to you.

Customers sometimes access retirement contributions from their investment account and delay submitting for the pension retirement—usually to start the pension income when they reach full retirement age, or to start an early retirement with an unreduced pension. See this two-minute video about delaying retirement.

Plan 3 customers also have the option to purchase the TAP Annuity using their Plan 3 investment account.

The time it takes to access your Plan 3 investment money can vary depending on where your contributions are invested. Find out more about withdrawing from your plan on your plan page.

Subscribe for more DRS news

In today’s climate of economic uncertainty and budgetary challenges, many public employees in Washington State are facing difficult decisions...

Our Retirement Specialists take calls from DRS customers who are often unaware they have retirement funds waiting for them in their accounts.

The 2025 Legislative session begins Jan. 13, 2025. We’re tracking retirement-related topics in the table below.