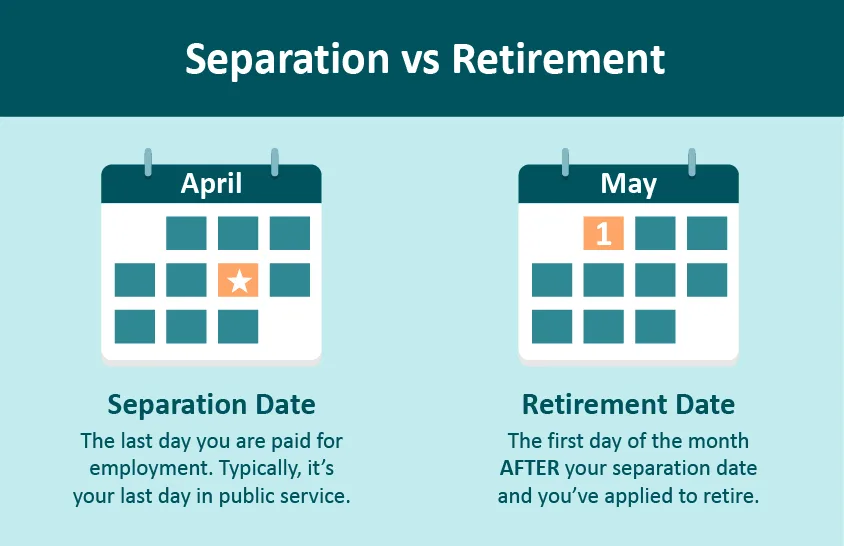

Leaving Employment

If you separate from DRS-covered employment, you can choose to either leave your contributions in the plan until you’re eligible to retire or withdraw them.

FAQ about leaving employment

How does leaving my job, taking a break between jobs or working in the private sector affect my retirement account?

You can do one of the following:

- Retire (if you’re eligible) and begin receiving your benefit

- Leave your money in your account until you’re eligible to retire

- Withdraw your account balance

Consider this:

- How close you are to retirement

- If you plan to return to a position covered by the same retirement plan

- Whether you are vested in your plan

- Other sources of income or savings

When will I be eligible to retire and collect a monthly benefit?

Once you have met the age and service requirements of your plan, you can retire and collect your benefit. Visit your plan page to review the service requirements under “When can you retire?”

What happens if I withdraw my retirement account money?

Plan 1 or 2: If you withdraw your funds, you’re required to withdraw the entire amount and you become ineligible to receive a retirement benefit.

Plan 3: You can withdraw your investment contributions and still receive a monthly benefit when you’re eligible to retire if you are vested.

Taxes: The law requires DRS withhold 20% federal income tax on all tax-deferred contributions and interest paid directly to you. If you’re younger than age 59½, you might also have to pay an additional 10% for withdrawing early when you file your taxes. The IRS can tell you whether this would apply to you. Taxes aren’t withheld on qualified rollovers.

Why might I want to leave funds in my retirement account?

Plan 1 or 2: If you’re vested and leave your money in your retirement account, you’re entitled to a monthly pension benefit for the rest of your life once you qualify. Your account will continue to earn interest until you retire or withdraw at a later date.

Plan 3: If you leave money in your investment contribution account, it can grow (subject to market conditions) while you keep control of your investment choices.

What happens to my account if I return to a public-sector job?

If you go to work for one of the approximately 1,400 DRS-covered employers and:

You retired: You might be able to work limited hours without affecting your benefit.

You left money in your retirement account or you’re a Plan 3 member: You’ll begin contributing to your retirement account again. Plan 3 members can withdraw their investment contributions but not the pension funds their employers contribute.

You withdrew from Plan 1 or 2: You will begin contributing to your account again. You will have the option to repay the money you withdrew plus interest to restore your service credit. This retirement benefit is a defined benefit based on your years of service as well as your earnings.

What options do I have regarding my DCP account?

If you retire or leave your public-sector job, you can leave your money in your Washington Deferred Compensation Program (DCP) account, or choose to receive some or all of your account balance. If you are age 73 or older, see required minimum distribution.

If you continue public employment, and your employer participates in DCP, you can continue, increase, reduce or stop your DCP contributions. In limited circumstances, the IRS allows hardship withdrawals while you’re employed.

If I withdraw my retirement funds, will they be taxed?

Yes. Payments you receive are subject to federal tax. To find out more about how taxes could affect you, contact a tax advisor.

Which employers participate in DRS-covered retirement plans?

See page 224 of this report for a complete list of DRS plan employers.

Former members

If you separate from employment, you can choose to either leave your contributions in the plan until you’re eligible to retire or withdraw them. The IRS requires that you begin taking payment of your monthly benefit by the time you are 73, unless you are still employed.

Be sure to keep your contact information and beneficiaries up to date even if you separate from service. You can do this instantly through your online account.

Inactive accounts search: Former members can check whether they have funds available using this tool.

More about how separation can affect your retirement:

Plans