DCP – Deferred Compensation Program

What is DCP?

The Deferred Compensation Program (DCP) is a special type of savings program that helps you invest for the retirement lifestyle you want to achieve—a lifestyle that might be hard to reach with just your pension and Social Security.

DCP is an IRC Section 457 plan administered by the Washington State Department of Retirement Systems (DRS). DCP is similar to a 403b program.

Regulations: DCP adheres to administrative codes or rules adopted by Washington agencies. See the DCP section of the WAC (Washington Administrative Code).

Easy

Contributions are automatically deducted from your paycheck, so saving is easy. Start with as little as $30 per month. You can also let your contributions grow with percentage deductions.

Flexible

Online or by phone, you can change your contribution amount and investment selections at any time. Your changes can take up to 30 days to go into effect (depending on your employer’s payroll cycle).

Smart

DCP offers a variety of professionally managed investment options, including “one-step” funds that automatically rebalance the asset mix as you move toward your target date for retirement. Funds are selected by the Washington State Investment Board, with fees among the lowest in the marketplace.

Investment Account Customer Service by Voya Financial

Voya Financial is the DRS record keeper for DCP, Plan 3 and JRA customer investment accounts. They can assist you with transactional needs and account information.

Call Voya: 888-327-5596 (TTY users dial 711)

Fax: 844-449-2551

Chat live with customer service when you select the chat icon from the Voya login page (you can also chat once you are logged into your investment account).

Mailing address:

Voya Financial

Attn: Washington State DRS

PO Box 389

Hartford, CT 06141

What does the record keeper do?

The DRS record keeper maintains the records for Plan 3, DCP and JRA customer investment accounts and assists customers with transactions related to these accounts.

Roth option

DCP now offers a Roth or pretax option. Each option affects when your retirement contributions will be taxed.

What is pretax? With the DCP pretax option, your contributions are made before tax. Withdrawals, including investment earnings, are taxed in the year of withdrawal.

What is Roth? With the DCP Roth option, your contributions are deferred from your already taxed income. Roth withdrawals, including any investment earnings, are not taxed if you meet the minimum qualifications. These include a five-year holding period from the year of your first contribution and a minimum age of 59½. If you withdraw before meeting these, any investment earnings will be taxed.

Compare pretax and Roth options

| Option | Pretax | Roth |

|---|---|---|

| Minimum contribution | $30 or 1% of your gross annual salary per paycheck, per option | |

| Maximum contribution | $24,500 (In 2026. See more on annual limits) | |

| Taxes on contributions | No, contributions are not taxed | Yes, contributions are taxed |

| Taxes on withdrawals | Yes, withdrawals including investment earnings are taxed | No, there are no taxes for withdrawals including investment earnings* |

| Conversions | No, you cannot convert DCP Roth dollars to pretax | Yes, you can permanently convert DCP pretax dollars to Roth |

| Rollovers | Yes, you can roll eligible pretax funds in or out | Yes, you can roll eligible Roth funds in or out (Roth IRA is not eligible) |

More about Roth and pretax options

How do I add Roth?

Existing DCP customers can add Roth by logging into your DCP account and making the change. Or you can contact Voya at 888-327-5596 for assistance.

New customers can enroll in DCP.

Can I convert a DCP pretax balance to Roth?

Yes. However, you will be responsible for paying any taxes due when you file your taxes at end of the year. Taxes will NOT be withheld by DRS or the record keeper at the time of the conversion. The converted amount will be reported to the IRS and to you on a 1099. If you make the conversion after mid-December, the converted amount would be included in your taxable income for the following year. See this short video about Roth conversions.

To convert your existing DCP pretax account to the Roth option, complete this conversion request form. For questions about conversions, contact the DCP record keeper.

Can I contribute to both Roth and pretax in DCP?

Yes. You can choose to contribute to both or either option. You’ll be able to review and access both balances using your online account. The combined contributions for both options must fall within IRS annual limits.

What is the minimum amount I can contribute?

For DCP (Roth and pretax) the minimum is 1% or $30. The contributions must be whole numbers. This means if you were contributing to both options, you’d be contributing at least 1% each to Roth and 1% to pretax. Or at least $30 as a combined minimum for both.

What is the maximum amount I can contribute?

The combined yearly total for both options (DCP Roth and pretax) must fall within the IRS limits for this account type. These limits are set annually by the IRS. If you are 50 or older, your annual limit is higher.

Can I contribute a percentage or dollar amount to Roth?

Yes, you can choose either a percentage or a dollar amount. If you are also contributing pretax dollars, you need to use percentages for both or dollar amounts for both, but the amounts you contribute to each can be different. Example: If you are contributing 3% pretax and you want to also contribute to Roth, you will need to select a percentage of 1% or more. Or you can change both contributions to whole dollar amounts.

How long will it take for my contribution changes to go into effect?

Any DCP contribution changes you make to your account can take up to 30 days to go into effect (depending on your employer’s payroll cycle).

Why might customers choose the Roth option?

Because you pay tax on the contributions, Roth offers a source for tax-free retirement income. If you expect your retirement income taxes will be higher than your current income taxes, Roth could save you money. Money withdrawn will not be taxed if your first contribution is at least five years old. Less tax on your withdrawals could mean more money in your pocket during your retirement. Your retirement savings needs may vary—talking with a financial professional can help you determine which option is best for you.

How is DCP Roth different from a Roth IRA?

The main difference is Roth IRA has income limits to participate. DCP Roth does not. DCP Roth also has higher maximum contribution limits than a Roth IRA.

Can I contribute to DCP Roth and a Roth IRA at the same time?

Yes. You can contribute to both, and the limits for a 457 account (DCP) and an Individual Retirement Account (IRA) are separate. We recommend you consult your financial advisor to determine your retirement planning needs. DRS and the record keeper, Voya, are unable to offer financial advice.

How is a Roth deferral percentage calculated from the paycheck?

The percentage is calculated from the total gross salary for the pay period, before any deductions are applied.

When does my Roth balance qualify for tax-free withdrawal?

A non-taxed withdrawal, also called a qualified distribution, is generally a withdrawal made after a 5-taxable-year period of participation, and is either: made on or after you reach age 59½, made on or after your death, or attributable to your being disabled.

Will I be taxed on the Roth contribution amount if I take a withdrawal before 5 years?

Yes, if it hasn’t been at least 5 years since your first taxed (Roth) contribution, the IRS considers your withdrawal an unqualified distribution and you will be taxed on the earnings associated with those taxed (Roth) contributions.

Are unforeseeable emergencies allowed from Roth?

Yes, but you may be taxed on earnings if it hasn’t been at least 5 years since the year of your first taxed (Roth) contribution into the plan.

Is the first Roth contribution date on the account used for calculating the 5 years for a Roth In Plan conversion?

Yes. The first taxed (Roth) contribution date is used.

If I take a Roth withdrawal and a pretax withdrawal, will I receive one or two 1099s?

You will receive two separate 1099s.

How will I claim a Roth withdrawal on my taxes?

If the withdrawal is qualified (meaning it meets the 5 year minimum and is made on or after age 59 ½), you do not include it in your gross income. If the withdrawal is nonqualified (meaning it doesn’t meet the criteria for being tax-free) you would report the non-qualified distribution to the IRS using form 8606.

Can I use my Roth balance to purchase an annuity (or additional service credit)?

No. The annuity payment is taxable income when you receive it. You can only use dollars from your pretax DCP balance. However, you can take a distribution from your Roth and use it to purchase additional service credit.

Can I choose different investment options for my Roth and pretax contributions if I contribute to both?

When you enroll in DCP, you will need to select the same investment options for both Roth and pretax. After you have enrolled, you can select different investments for your Roth and pretax contributions through your online account.

My employer contributes to my DCP account. Will these funds go to my Roth or pretax balance?

Your employer’s contributions will be pretax. If your employer provides matching funds and you contribute to a Roth account, your employer’s contributions will still be pretax.

Can I change my mind and have designated Roth contributions treated as pretax contributions?

No. Once you designate contributions as Roth contributions, you cannot later change them to pretax contributions.

Will automatically enrolled new hire contributions continue to be tax-deferred (pretax)?

Yes. The default contribution for automatic enrollment will still be 3% toward the DCP pretax balance. New employees can elect to participate in either or both pretax and Roth. Changing the account type, investment option or contribution amount, will make you an active participant (which means you can no longer withdraw any contributions made during automatic enrollment).

Can I roll over my Roth account balance if I change employment?

Yes. You have the option of rolling out dollars from your Roth 457(b) account to a Roth IRA or another employer plan with designated Roth accounts (such as a 457, 401(k) or 403(b)) that accepts Roth rollovers). Likewise, your DCP account accepts pretax and Roth rollovers-in from eligible plans.

Where can I find more about DCP Roth?

Reach out to the DCP record keeper, Voya Financial for additional information.

DCP calculators

DCP Savings

Use this calculator to estimate future potential DCP savings. Find out how much you can save, withdraw and how long your money will last.

Compare Roth and pretax

Use this calculator to compare your savings options when deciding whether to contribute to DCP pretax, Roth or both.

Enrollment

Enrolling as a new customer is easy! First make sure you’re eligible for Washington’s DCP by talking to your employer or reviewing this list of eligible employers. Then enroll online using this web form.

New DCP customers can also enroll by completing and mailing this paper form. If you are already enrolled in DCP, do not use this form. To change contributions, add Roth or opt out of automatic enrollment, make the change through your online DCP account or contact 888-327-5596.

Reenrolling in DCP

If you leave employment and later return to a DCP-covered employer, resuming your DCP contributions is easy. Complete a new DCP enrollment request using the options above!

Automatic enrollment for new hires

New employees: Have you received a letter about being automatically enrolled in DCP? Because DCP is voluntary, there are actions you can take once you receive your enrollment notification letter in the mail. For example, you can change your contribution amount or your investment options. You can also opt out of DCP with the option to rejoin later.

How much time do I have to make a decision about DCP automatic enrollment?

Enrollment timeline

- Day 1 You are hired

- About 30 days after hire You receive a mailed DCP notification letter (the timing is dependent on your employer’s payroll cycle)

- Within 30 days of date on notification letter You have 30 days to opt out of DCP enrollment if you do not want to participate

- 2 months after your hire date Your 3% paycheck contributions begin if you make no changes to your DCP account

- Within 90 days of your first contribution You can still withdraw your automatic enrollment contributions and stop your deferrals.

Example: Someone hired in February will begin DCP contributions in April and will have until July to stop and withdraw these contributions - 90 days after your first contribution At any time during your employment, you can change or stop your contributions, and you can change investment options. Only normal withdrawals are permitted after this point (normal withdrawals are when you leave DCP-covered employment).

Frequently asked questions about automatic enrollment

Why have I been enrolled?

Your organization participates in automatic enrollment.

Are any employees exempt from automatic enrollment?

Yes. Automatic enrollment does not include student employees or retirees returning to work, even if they fit the newly hired/full time employee status.

How do I change my DCP options or opt out of automatic enrollment?

Once you receive a DCP notification letter you can choose to opt out, change your contribution options or select another investment. Make these changes through your online account or call 888-327-5596.

How much will I contribute with automatic enrollment?

3% of pretax income is the default deferral rate.

When will I make my first contribution?

Approximately two months after your hire date. The time varies due to your employer’s payroll cycles. Changes made during the initial automatic enrollment period make you an active DCP participant, which means your contributions may begin sooner AND you can no longer withdraw any contributions made under automatic enrollment.

What kinds of changes make me an active participant?

If you change your investment option or contribution amount, this will make you an active participant (which means you can no longer withdraw any contributions made during automatic enrollment).

Can I make changes after the opt-out deadlines have passed?

Yes. At any time during your employment, you can stop your deferrals or change your contribution amounts. You can also change investment options.

Where will my contributions be invested?

Your contributions will be invested in the Retirement Strategy Fund that assumes you’ll begin withdrawing funds at age 65.

If I opt out, can I join DCP later?

Yes.

Can I withdraw contributions made during automatic enrollment?

Yes. If you make this choice within 90 days from your first contribution, you can withdraw your contributions from DCP as long as the record keeper receives your withdrawal request within the 90 days. These funds are not eligible for a rollover as long as you are actively employed. Log into your account or contact the DRS record keeper at 888-327-5596 to request a withdrawal.

Are my contributions subject to tax withholding if withdrawn?

Yes, because your contributions are pretax dollars. The tax withholding is 10%. You will receive a 1099 tax statement for the year of the withdrawal. DCP doesn’t have early withdrawal penalties.

Also see this automatic enrollment flyer.

Contributions and limits

Limits

With DCP, you can change your contributions at any time. This includes starting, stopping, increasing or decreasing the amounts you contribute from your paycheck. Contribute to your DCP account in dollar or percentage amounts. The choice is yours.

These limits apply to Roth and pretax contributions. This means whether you contribute to Roth, pretax or both, the combined totals must fall within IRS annual limits for the DCP 457(b) program.

Limits for 2026

Minimum monthly contribution: $30 or 1% of your earnings

Maximum annual contributions:

Under age 50: $24,500

Age 50 and over: $32,500 (see catch-up options)

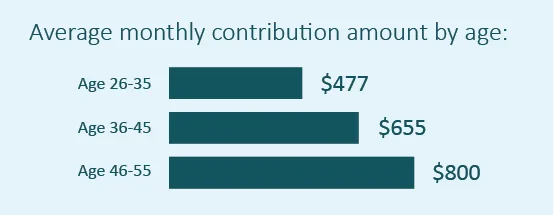

One in 20 DCP customers reach the annual maximum limit each year. If you are curious, here are some average amounts saved by age group.

Catch-up options

Participants age 50 and older: You’re allowed an additional $8,000, for a maximum limit of $32,500. For high income employees ($150,000 in FICA wages in 2025), the additional $8,000 may be required as Roth contributions.

Special Catch-up limit: You could contribute up to $49,000 annually when you’re within three years of retirement. To determine your eligibility, contact DRS.

At this time, DRS is not implementing the optional SECURE 2.0 Act provision that increases catch up contributions for individuals age 60 to 63.

Find out more about catch-up options in this short video.

Changing and stopping contributions

To change your contribution amount, log in to your account. From the DCP account page, select Change Monthly Contribution, Transactions. Your changes can take up to 30 days to go into effect (depending on your employer’s payroll cycle). If you separate from employment and later return to work for an employer who participates in DCP, you can reenroll anytime. If any payments from your account have started, they will stop. Estimate contributions with the DCP calculator.

Can I continue contributing to DCP after I separate from employment? No, once you separate from service you can’t continue contributing to DCP.

Your DCP contributions can be a percentage of your salary or a whole dollar amount. The choice is yours. This video talks a bit about why some customers choose a percentage contribution option.

Contributing cashed-out leave to DCP

If your employer provides compensation for unused leave, such as annual or sick leave, consider deferring these cash-outs into DCP to maximize your contributions. Annual maximum limits apply, and your employer must participate in DCP for you to be eligible. You can choose DCP Roth, pretax, or both for your contributions. Consult a tax advisor for information about federal income taxes on your contribution. DRS is unable to offer tax advice. Current enrollment in DCP is not necessary.

How to contribute your leave to DCP

Complete the following steps at least 30 days before you are paid your cash-out leave. The IRS requires that you complete the deferral form before your last day of employment.

First, you’ll need this information from your employer’s payroll office:

- The dollar amount of your leave cash-out eligible for DCP deferral (after applicable withholdings such as Social Security and Medicare). Be sure to deduct federal income tax for Roth contributions and confirm the dollar amount before you decide to contribute all or a portion of your leave to DCP.

- The date the leave cash-out will be paid.

Next, complete the DCP Lump Sum or Leave Cash-Out Deferral form and submit it to DRS.

- The amount you put on this form will be withheld. Confirm the amount with your employer so you have enough leave to cover your contribution request.

- The form can take 10 business days to process. You and your employer will receive a confirmation email when the deferral is setup.

- To update the deferral amount, submit a new form. Requests or changes made less than 30 days before the pay date may not be processed in time. The IRS requires that we receive the form before you separate from employment.

Note: If your participation in VEBA (Voluntary Employees’ Beneficiary Association) is funded by sick leave cash-outs, those funds may not be directed to DCP. Please check with your payroll or human resources department to verify VEBA participation and how it is funded.

Rollovers

What is a rollover? A rollover is moving funds from one eligible retirement plan to another. Rollovers can include a rollover out (moving funds out of an account) and a rollover in (moving money into an account).

You can roll out your pension account contributions, DCP and Plan 3 investment balances at any time once you separate from service. Pension plan contributions made by your employer are not eligible for rollovers. These dollars remain in the pension trust fund and are only available to you as part of a monthly pension retirement income.

While DRS doesn’t charge fees for rollover services, your other financial institutions could. Make sure you’re aware of any fees or differences in expenses, options and services before you move your funds. We recommend initiating your withdrawal/rollover promptly because your institution’s withdrawal timelines can take weeks or months. If DRS doesn’t receive your funds by the bill due date, your rollover will not be accepted.

Converting a cash withdrawal to a rollover

If you make a cash withdrawal, you’ll have 60 days from the date you receive payment to deposit the funds into a traditional IRA or another eligible plan that accepts rollovers. Your rollover in amount must match the rollover out amount before taxes or the difference is subject to income tax. You may choose to pay the difference out of pocket when you roll it over. This difference could be recovered when you file your annual tax return with the IRS. Consult your tax advisor or visit this IRS page to find out more.

Rolling funds out of DCP or JRA

Once you separate from service, you can request a rollover of your DCP or JRA balance through your online investment account. The DRS record keeper, Voya Financial will process the rollover. You will be mailed the check made out to your selected rollover recipient, and you will need to provide them this check. For assistance, contact Voya at 888-327-5596.

If you roll your DCP funds directly over into a traditional IRA or eligible retirement plan, the funds won’t be taxed until you withdraw them. If you roll over into a Roth account, the rules could be different. Check with the IRS to learn how this choice will impact you.

Rolling funds into DCP

DCP can accept rolled funds from previous employers held in eligible retirement plans such as 457(b), 401(k), 403(b) and traditional, pretax IRA accounts. The IRS prohibits rolling Roth IRAs into DCP.

DCP is the only DRS administered plan that accepts rollovers from other plans. The rolled-in funds will retain the tax rules they come in with.

Rolling funds into DCP requires two steps:

- You must be enrolled in DCP. If you’ve left public service, your DCP account will need to still have a balance in order to roll in additional funds.

- Submit a completed rollover-in form prior to sending us a check.

If you are rolling eligible Roth funds into DCP, you’ll need to know the date you started contributions for the account. Ask your financial institution to provide these details.

Withdrawals

Eligibility

For most customers, you must be separated from DCP-covered employment to withdraw from your account. If you submit a withdrawal request while you are still employed, the request will be held for up to 180 days until we receive a separation date from your employer. Once you separate, the funds will be released to you. It’s common for your employer to submit your DCP separation date after they report your retirement plan termination date.

How to withdraw from DCP

To complete your withdrawal online, log into your online account and select your DCP account. Under the “More resources” menu, select Request online withdrawal.

With online withdrawal, your account information is prefilled for you, you can estimate payments and tax withholdings and add your direct deposit information. You’ll also receive immediate confirmation that your transaction is in progress.

You can also contact the DRS record keeper, Voya financial at 888- 327-5596 for assistance with your investment transaction. Log into your DCP account to chat live with a customer service associate. They will help you select the right transaction for your needs.

What withdrawal types are available for DCP?

- DCP Withdrawal – This is the withdrawal type you can make when you separate from employment. The withdrawal offers you a variety of options for payment types including lump sum, installments and rollovers.

- DCP In-Service Withdrawal – This type of withdrawal allows you to make DCP withdrawals while you are still employed. See the below section “Can I withdraw from DCP while employed?” for eligibility information.

- RMD Change Request – Customers who receive a required minimum distribution (RMD), use this form to request changes to your annual minimum distributions. More about required minimum distributions.

- Beneficiary Distribution Request – Request a withdrawal from your awarded beneficiary account.

- Alternate Payee Withdrawal – Withdraw funds per a Qualified Domestic Relations order.

- Unforeseeable emergency withdrawals – If you are experiencing severe financial hardship because of an unforeseeable emergency, you may be eligible to withdraw funds from your DCP account. IRS requirements restrict this type of withdrawal, and may limit the amount you can withdraw.

- Automatic Enrollment Withdrawal – New employees automatically enrolled in DCP have up to 90 days after their first paycheck deferral to cancel DCP and withdraw any contributions. After 90 days, standard withdrawal eligibility applies.

More DCP transactions

- Direct Deposit – Request or modify direct deposit for your DCP, Plan 3 or JRA investment account payments.

- IRS Form W-4P – Request to have federal income tax withheld from each withdrawal or annuity payment you receive.

Can I withdraw from DCP while employed?

In some cases, you can withdraw your DCP funds while you are still working for a DCP-covered employer. Here are those exceptions:

- Unforeseeable emergency withdrawals: If you are experiencing severe financial hardship because of an unforeseeable emergency, you may be eligible to withdraw funds from your DCP account. IRS requirements restrict this type of withdrawal, and may limit the amount you can withdraw. See more about DCP emergency withdrawals.

- Automatic enrollment withdrawal: New employees automatically enrolled in DCP have up to 90 days after their first paycheck deferral to cancel DCP and withdraw any contributions. After 90 days, standard withdrawal eligibility applies. For more information, call 888-327-5596.

- De minimus request: If you have not contributed to DCP in at least 24 months, and your account balance is under $5,000, you can request a one-time withdrawal of these funds. For more information, call 888-327-5596.

- Age 59 1/2 or older distribution: If you are age 59 1/2 or older and you wish to withdraw or rollover from your account while you are employed, you can. To complete this withdrawal online go to your DCP account, select Loans & Withdrawals, Request a Withdrawal and choose the withdrawal type. Or call the DRS record keeper at 888-327-5596.

- Withdrawing rolled-in contributions: If you rolled funds from another plan or program into your DCP account, you can withdraw these funds. Keep in mind that these funds still carry any tax requirements or early withdrawal penalties they arrived with when you rolled them in. To complete this withdrawal online go to your DCP account, select Loans & Withdrawals, Request a Withdrawal and choose the withdrawal type. Or call the DRS record keeper at 888-327-5596.

- Plan-to-Plan Transfer: If your employer offers more than one 457 deferred compensation program, or the employer switches to another 457 program, you can transfer your Washington DCP funds to the other 457 program while you are still employed. To make this request, contact the DRS investment record keeper, Voya Financial, at 888-327-5596.

DCP emergency withdrawals

Emergency withdrawals, sometimes called unforeseeable emergency distributions, are certain hardship conditions where a customer can withdraw DCP funds while they are still working. The DRS record keeper, Voya Financial works with customers to process these claims and any resulting DCP distributions.

More about DCP emergency withdrawals

Two things you should know:

- The criteria of an unforeseeable emergency for DCP is set by the IRS. Any distributions must adhere to these rules.

- Knowing what an unforeseeable emergency is now could prevent some complications for you in the event a hardship occurs.

For example, credit card debt is not a qualified unforeseeable emergency. Even if the card was used to pay for a medical emergency. For us to approve the distribution, the need must be outstanding. While emergency medical bills could be approved for distribution, a credit card bill for those same bills would not.

How to request an unforeseeable emergency withdrawal from DCP

You can apply online or by phone.

Apply online: Log in, go to your DCP account, select Loans & Withdrawals, Request a Withdrawal and choose the withdrawal type.

Apply by phone: Contact the DRS record keeper, Voya Financial at 888-327-5596 when the emergency occurs. Inform them of the need to withdraw funds from your DCP account.

What’s next? Voya will provide you with instructions on what actions are needed next. You’ll need to gather documentation to support your claim. Copies of bills, invoices, quotes—documentation is more than a letter written by you.

Here are some situations where the unforeseeable distribution may or may not apply.

These could be unforeseeable emergencies:

- An illness or accident affecting you, your spouse, or your dependent

- Loss of your property due to casualty (including the need to rebuild a home following damage to a home not otherwise covered by homeowner’s insurance, e.g., as a result of a natural disaster)

- The need to pay for the funeral expenses of your spouse or dependent

- Imminent foreclosure of, or eviction from, the participant’s primary residence

- Other similar extraordinary and unforeseeable circumstances arising as a result of events beyond the control of the participant

In all of these cases, you must be able to prove you are NOT able to cover the cost without the DCP withdrawal.

These are NOT unforeseeable emergencies, and cannot be used as reason to request a DCP withdrawal:

- Credit card debt (even if the debt is from paying for an emergency)

- Buying a home

- College tuition

- Student loans

More about unforeseeable emergency withdrawals

IRS unforeseeable emergency distribution information

Washington Administrative Code: Unforeseeable emergency withdrawals

If the DRS record keeper, Voya Financial denies your request for distribution, you’ll receive a letter with instructions to request further review by DRS if you wish. See additional information.

Beneficiaries

In the event of your death, your beneficiaries will receive payment from your DCP account. Keeping your beneficiaries updated is important. Your DCP beneficiaries must be declared separate from any beneficiaries you’ve selected for another plan or program, like a pension. You can name anyone as your beneficiary: spouse, child, domestic partner, friend, neighbor, etc. You can also designate a charity or trust. If you die without a current beneficiary designation on file, a distribution will be made to your estate.

Once you are enrolled in DCP, update your beneficiaries online through www.drs.wa.gov/oaa. Or complete the paper form (Beneficiary Designation) and mail it to DRS. See the Forms section of the DRS website.

Information for beneficiaries

The DCP account holder (participant) selects one or more beneficiaries. When DRS is notified of the participant’s death, we mail a letter and beneficiary form to each beneficiary on file. Once the form is returned to DRS, we set up a separate account under the beneficiary’s Social Security number. This account is called a “beneficiary account.”

When you contact us, please be ready to provide the deceased participant’s:

- Full name

- Social Security number

- Date of death

Common questions we receive about beneficiary accounts

What are my withdrawal options?

If you are a spouse, you have the same withdrawal options as the participant did. You can leave the money in the account, withdraw in full or withdraw it in payments. If you are not a spouse, you can withdraw the funds. For more specific information about withdrawal options, contact the DRS record keeper.

Can I contribute additional funds to the awarded beneficiary account?

No.

Can I roll my beneficiary account funds into my IRA?

A spouse beneficiary can roll the funds into a traditional IRA. A non-spouse can roll the funds into an inherited IRA.

Can I roll my awarded beneficiary account into my own DCP account?

No. The accounts must be kept separate for distribution purposes. However, you can withdraw the beneficiary account funds while you are still working for a DCP-covered employer.

How do I name a beneficiary for my awarded beneficiary account?

You can’t. Upon your death, any remaining funds go directly to your estate.

Who can I contact?

For more information about beneficiaries, contact DRS.

Investments

DCP and JRA customers have investment accounts. We offer two types of funds: One-step or build and monitor. All funds are managed by the Washington State Investment Board.

One-step: These investments are automatically adjusted for you based on your age. The One-Step Investing approach includes Retirement Strategy Funds, also called age-based or target date funds. Because most customers choose one-step investing, this is also the default investment type for customers who do not select investments.

Build and monitor: This is the DIY approach to investing where you choose from a selection of investments and create your own mix from a list of funds.

Investments and fees

Select the funds below to view their fact sheets. Funds for each table are listed in order of risk (lowest to highest). View the latest performance for all funds through your online account. The management fees associated with each fund are included here. These costs are in addition to the administrative fees detailed in the table lower in this section.

Retirement Strategy Funds (Fees as of July 2025)

Build and monitor funds (Fees as of July 2025)

| Funds | Manager fee |

|---|---|

| Savings Pool Fund | 0.004% |

| Washington State Bond Fund | 0.007% |

| Socially Responsible Equity Investment | 0.42% |

| U.S. Large Cap Equity Index Fund | 0.001% |

| Global Equity Index Fund | 0.035% |

| U.S. Small Cap Value Equity Index Fund | 0.018% |

| Emerging Market Equity Index Fund | 0.09% |

Investment performance

View or compare the most recent performance for your DCP investments through your online account. You can also access a quarterly overview of fund performance in the table links that follow.

Administrative fees (as of July 2025)

| Fee Type | Percentage |

|---|---|

| WSIB fee | 0.0167% |

| Recordkeeping fee | 0.0560% |

| DRS administrative | 0.030% |

Investments have two types of costs. The management cost for the individual investment and the administrative costs applied to all plan investments. This table includes the administrative costs in addition to your fund fee in the previous tables. Find out more about investment costs in this video or in the investment faq section.

Managing your investments

Make investment changes through your online account. Change your fund selections anytime during or after your employment. You can also contact the record keeper for assistance.

Trading restrictions:

To safeguard customers against the effects of excessive trading, DRS has established trading restrictions that regulate how frequently you can change investments.

If you are transferring more than $1,000 out of a fund, you are required to wait 30 calendar days before transferring money back into that same fund. The 30-day window is based on the last time you made a transfer out of the fund. The restriction will not affect your regular contribution or the ability to leave state service and withdraw your money. Transfers of $1,000 or less are not impacted by the trading restrictions.

DRS periodically reviews trade data to identify excessive trading. If existing restrictions are not sufficiently addressing excessive trade practices, DRS might take additional action. DRS reserves the right to establish or revise restrictions to comply with federal or state regulations, or as circumstances indicate.

In addition to the trading restrictions described above, DRS will also comply with restrictions put in place by our fund managers.

Note: Excessive trading (also referred to as “market timing”) involves transferring significant amounts of money and/or making frequent trades between investment options. This practice requires more cash on hand to honor the frequent trades and transfers. Because the excess cash is used to cover potential transfers instead of being invested, long-term returns can be lowered for other participants. Excessive trading can also increase fund management costs.

Investment FAQ

Can DRS tell me what to invest in?

No. While DRS and the DCP record keeper can provide information about investments, we cannot offer investment advice. Find out more about each fund by reviewing the fact sheet linked to the fund name in the investments and fees section. These fact sheets are prepared by the fund managers and contain information about performance, asset mixes and the goals of the fund. If you aren’t sure which investment approach might be right for you, talk with your financial advisor.

How do I choose a one-step Retirement Strategy Fund?

Take your birth year and add the age you expect to retire. That gives you a target year. Then you pick the fund with the date closest to that year.

Example: If you were born in 1993 and want to retire at 65 → 1993 + 65 = 2058 → pick the 2060 fund.

Are there fees with DCP investments?

Yes, but they’re pretty low. Even though investment fees are often small (fractions of a percent), they do add up over time. It’s good to know the cost differences when you compare investment options as well. DCP has two types of fees:

1. Administrative Fees

These cover fund costs like recordkeeping, communications, customer service, and oversight by the Washington State Investment Board (WSIB).

- The total WSIB, DRS and recordkeeping admin cost for DCP is 0.1027% per year.

- These fees are listed on your quarterly statements under “Expenses.”

- This fee is reviewed annually and may change each July.

2. Management Fees

These are what you pay the professionals who manage the funds. Review the management fees within the fund fact sheets linked in the investments and fees section.

- The amount varies depending on the fund you choose.

- Unlike admin fees, these are included in the share price and not shown on your statement.

- You can switch your investment choices at any time, and it’s smart to check the management fee before making changes.

Example:

Let’s say you have $10,000 in the 2035 Retirement Strategy Fund. Here’s how the annual fee breaks down:

- 0.21% (Fund manager fee)

- 0.0167% (WSIB admin fee)

- 0.0560% (Recordkeeping admin fee)

- 0.030% (DRS administrative fee)

- Total: 0.3127%

So, $10,000 x 0.003127 = $31.27 per year in fees.

What is fund risk, performance and diversification?

Here’s the quick rundown:

Risk: All investments carry some risk. Generally, younger folks can handle more risk (more growth potential), while people nearing retirement often choose safer options. How much risk you take is really up to you.

Performance: Past returns aren’t a promise for future ones, but they can show how the fund tends to behave.

Diversification means spreading your money around, like not putting all your eggs in one basket. That way, if one investment drops, others might balance it out.

- If you go with a Retirement Strategy Fund (the “One-Step” option), it’s already diversified and will adjust automatically as you get closer to retirement.

- If you want more control (the “Build and Monitor” route), you can mix and match between different funds.

Can I invest in funds that aren’t listed here?

No. DRS does not offer a brokerage account option, and you must select from the lineup available. Each fund typically includes a mix of investments, such as stocks from various companies. You can review the fact sheets in the available investments section to see a summary of what’s included in each option.

All investment options for DRS plans are selected by the Washington State Investment Board (WSIB). If there are funds you would like to see, you can submit public comment to WSIB.

Where can I get more information about investing?

Investment fee comparison

Compare how investment fees can impact your account using this calculator.

Investment basics webinar

This DRS recorded webinar explores the investment options available to DCP and Plan 3 customers.

Financial Literacy and Education Commission

MyMoney.gov promotes financial literacy and education. Find out how to plan for life events with financial impacts, such as birth or adoption of a child, home ownership or retirement.

U.S. Securities and Exchange Commission (SEC)

The SEC provides investment regulation and education.

Washington State Department of Financial Institutions (DFI)

DFI provides regulatory oversight for our state’s financial service providers.

Washington State Investment Board (WSIB)

WSIB closely monitors the performance of all DCP investment options.

Required minimum distribution

What is a required minimum distribution (RMD)?

If you are a DCP customer who is separated or retired, you must withdraw a minimum amount from your retirement investment accounts every year starting when you reach age 73. This minimum distribution of funds is required by federal income tax regulations. DRS calculates and pays out the minimum amount to you each year. This is to help you avoid the 25% tax penalty the IRS can impose if the minimum is not withdrawn.

The payments are automatically distributed to you, so no actions are needed for you to meet the requirements. But you can also choose to make adjustments to the distribution, such as the frequency of payments. Here is the form you need:

If you are still employed under a DCP plan, you are not required to take an annual Required Minimum Distribution. However, you can choose to withdraw the RMD amount once you reach age 73. You can do so online.

Note: The SECURE Act has raised the RMD age from 70 ½ to 73 for most retirees. However, retirees born before July 1, 1949 will still have an annual RMD starting in 2021. DRS recommends that you consult a tax advisor for information on how the new RMD legislation affects you.

How is the minimum payment calculated?

You can calculate your required minimum distribution by taking the previous year’s Dec. 31 investment account balance and dividing it by the IRS distribution period based on your age. If you are a member of Plan 3 and DCP, you have two investment accounts that are subject to minimum distribution requirements and you calculate these separately.

To calculate your own RMD withdrawal, use the table linked below. Find your age in the table. The distribution period is the number you divide your total investment account balance by to get the required minimum amount.

IRS distribution period for your age

See the IRS distribution period for your age.

This table applies to you if your status is:

- Unmarried

- Married with spouse who is not more than 10 years younger

- Married with spouse who is not the sole beneficiary of your account

Example of an RMD calculation:

Alex is age 75 with a DCP account balance of $150,000 as of December 31, 2018. To find the required minimum distribution (RMD) amount, Alex takes the account balance and divides it by the distribution period based on age 75, which is 22.9 years.

$150,000 / 22.9 years = an RMD of $6,550.00 for 2019.

If Alex is also a member of Plan 3, the same calculation will need to be performed on the Plan 3 investment account balance.

When is it due?

DRS must issue your minimum payment by Dec. 31 to meet IRS requirements. You’ll usually receive your payment earlier in December. DRS sends reminders each year to all RMD eligible customers. In the years after age 72, these payments will be automatic. You can change the frequency and amount of payment anytime by completing a DCP withdrawal. Your withdrawal amount must at least meet the required annual minimum.

How do the requirements apply to a surviving spouse or beneficiary?

If the original account holder dies, the required minimum distribution is still required for beneficiaries of the account. Here’s how these requirements work:

A spousal beneficiary will be required to continue receiving RMD payments if the account owner had already met the required age. If the account owner had not reached the required age prior to death, the spousal beneficiary will be required to start their RMD payments in the year in which the account owner would have turned age 72.

For non-spousal beneficiaries, the RMD is calculated based on the beneficiary’s life expectancy in the calendar year immediately following the account owner’s date of death. DRS will process an RMD payment if the account owner had turned age 72 or older. If the account also has rollover requests, the RMD will be processed before these.

What if I’m still employed?

If you are still employed by the same DRS-covered employer, the minimum distribution requirement does not apply to you. If you separate from your DCP covered employment and you are age 72 or older, the RMD will apply.

For DCP customers, if you are age 72 or older, you can withdraw your required minimum distribution amount even if you are still employed. Complete the RMD change request form.

What about Plan 1 and Plan 2 members?

Plan 1 and Plan 2 pensions are paid from retirement trust funds and are not subject to minimum distribution requirements. As noted above, RMD rules do apply to DCP accounts. If you have any other investments outside of your Plan 1 or Plan 2 pension account, you may be required to withdraw from those accounts.

More information

To find out more, contact the DRS record keeper at 888-327-5596 or visit the RMD section of the IRS website.

This information about required minimum distributions is a summary. For a complete description of RMD rules and information, see Required Minimum Distributions on the IRS website. If a conflict exists between the information on this page and what is contained in current law, the law governs. Please talk with your financial advisor if you have questions about taxes on your investment funds. DRS team members aren’t able to give tax advice.

Taxes

Do you pay taxes on DCP withdrawals?

Pretax contributions

Yes. You will pay federal income taxes on any pretax withdrawal from your DCP account. If you choose a lump sum or partial lump sum to be paid directly to you, or receive payments over a period of less than 10 years, 20% of your distribution will be withheld for federal income taxes. If you choose an installment period of 10 years or more, your payments are considered ordinary income in the year they are issued.

Roth contributions

No, if you meet requirements. You make these contributions with taxed income, so you don’t pay taxes when you withdraw them. However, Roth does have some requirements for you to qualify for tax-free investment earnings. These include a five-year holding period from the year of your first contribution and a minimum age of 59½. If you withdraw before meeting these, any investment earnings will be taxed.

Federal Tax Saver’s Credit

Also called a Retirement Savings Contributions Credit, you might qualify for this tax savings. With this credit, you can write off a portion of your annual contributions. Visit the IRS website to see the income limits as well as eligibility information for this opportunity. For specific tax information, consult your tax advisor.

Managing your account

You can make DCP account changes anytime through your online account.

Access your account to:

- View your DCP balance

- Change your contribution amounts

- Choose Roth, pretax or both contribution types

- Change your investment elections

- Transfer account balances between investment options

- See fund performance

- Withdraw funds from DCP

You’ll receive a quarterly statement with performance information for your investment account.

Your statements will be available through your online account unless you opt into mailed statements through the record keeper.

Quarters are divided into the following months:

- First: January through March

- Second: April through June

- Third: July through September

- Fourth: October through December

Your statement could include information for more than one plan, depending on your situation. Quarterly statements are released within two months of the quarter-end.

More resources

- Investment account service

- Enrollment Guide (PDF)

- DCP calculator

- DCP webinar video (35 minutes)

- More DCP webinars