TRS Plan 3

Teachers’ Retirement System (TRS) Plan 3 is a 401(a) plan with two parts: pension and investment. Your employer contributes to your lifetime retirement pension, and you contribute to the investment account.

When you meet plan requirements and retire, you are guaranteed a monthly benefit for the rest of your life from the employer-funded pension. With the investment part, you choose when to begin withdrawing funds, which can be any time after you separate employment.

You contribute between 5% and 15% of your wages to your investment account. You select this percentage when you begin employment.

More about Plan 3 contribution rates

Member contribution rate options

Option A 5% all ages

Option B 5% up to age 35 6% ages 35 through 44 7.5% ages 45 and older

Option C 6% up to age 35 7.5% ages 35 through 44 8.5% ages 45 and older

Option D 7% all ages

Option E 10% all ages

Option F 15% all ages

If you don’t choose a contribution rate, your withholding will default to Option A. Once your rate is set, you can change it only when you change Plan 3-covered employers. Changing means working for a different employer, not another division or department within your current workplace. More about contributions.

Investment Account Customer Service by Voya Financial

Voya Financial is the DRS record keeper for DCP, Plan 3 and JRA customer investment accounts. They can assist you with transactional needs and account information.

Call Voya: 888-327-5596 (TTY users dial 711)

Fax: 844-449-2551

Chat live with customer service when you select the chat icon from the Voya login page (you can also chat once you are logged into your investment account).

Mailing address:

Voya Financial

Attn: Washington State DRS

PO Box 389

Hartford, CT 06141

What does the record keeper do?

The DRS record keeper maintains the records for Plan 3, DCP and JRA customer investment accounts and assists customers with transactions related to these accounts.

See a live or recorded Plan 3 webinar.

How much will your pension retirement be?

Estimate your retirement benefit in minutes using the personalized Benefit Estimator in your online account. Your total pension amount is based on your years of service and your income. See more about how we calculate your benefit.

How to estimate your benefit

-

- From the DRS homepage, select the Member Login button in the top right.

- Log in to your online account.

- In the menu bar, select your plan name – such as PERS 2. This will open a dropdown menu.

- Select Benefit Estimator.

- Read how to use the estimator and select Accept & Continue.

- For first-time users, we recommend using the four-step process. This helps you learn how your benefit is calculated.

You can use this tool at any point in your career. You can create an estimate using different factors as many times as you like. This calculator will allow you to see a private preview of what your monthly retirement income might look like.

Years of service

Review your service credit detail through your online account. Service credit is based on the number of hours you work, which your employer reports to DRS. You can earn no more than one month of service credit each calendar month, even if more than one employer is reporting hours you work. A school year spans Sept. 1 through Aug. 31.

You earn 12 months of service credit if:

- You work 810 hours or more, beginning work in September and working at least nine months of the school year. Note: If you retire before Aug. 31 of the school year, you will not receive full service credit for the year. For example, if you retired July 1, you would not receive service credit for July or August of that year because you were retired in those months.

What if you work fewer than 810 hours?

Work between 630 and 809 hours, beginning in September, and working at least nine months of the school year

You earn: Six service credit months (half a service credit for each month) per school year

Work at least 630 hours during at least five months within a six month period during the school year

You earn: Six service credit months per school year

Work 90 or more hours in a month

You earn: One service credit month per month

Work at least 70 hours but fewer than 90 hours

You earn: Half a service credit month per month

Work more than 0, but fewer than 70, hours

You earn: One-quarter service credit month for each month

More information about service credit

Items that could affect your service credit:

- Membership in another plan administered by Washington state.

- If you work as a substitute.

Employees of the Washington State School for the Blind, the Center for Childhood Deafness and Hearing Loss, or an institution of higher learning:

If you begin working in September in an eligible position and earn compensation during at least nine months of the school year, you can receive 12 service credit months for the school year if you are compensated for at least 810 hours of employment. Six service credit months can be awarded if you start in September and are compensated for at least 630 hours but fewer than 810 hours during the school year.

If you earn compensation in fewer than nine months of the school year, you will receive service credit based on the number of hours you are compensated for each month.

More about service credit.

Your income

The Average Final Compensation, or AFC is the average of your 60 consecutive highest earning months in your career. This could be at the beginning, middle or end of your career. DRS uses your AFC income information to calculate your pension amount. For high income public employees, federal law limits the amount you can contribute toward retirement and limits the benefit calculation. See IRS limits.

TRS Plan 3 pension formula

1% x service credit years x Average Final Compensation = monthly benefit

Example:

Let’s say you work 23 years and the average of your highest 60 consecutive months of income (AFC) is $5,400 per month.

1% x 23 years x $5,400 = $1,242

When you retire, you’d receive $1,242 per month in pension income. Remember, your investment income is calculated separately.

How much will your investment retirement be?

The total amount available from your investment account in retirement will depend on a few things.

- The income percentage you chose (or defaulted into) when you selected the plan

- Your income and years of contributions

- Investment selection and performance

Get a complete picture of your projected retirement income through your investment account. Here you can add your Plan 3 pension and investment income, social security, and any additional retirement savings such as DCP.

When can you retire?

Now that we’ve discussed how much money you can get in retirement, let’s talk about when you can retire. You are eligible for a pension retirement when you are vested, which happens when you have achieved one of the following:

- 10 service credit years

- Five years of service credit with at least 12 months earned after age 44

- Five service credit years earned in TRS Plan 2 before July 1, 1996

Full retirement

Full retirement is the earliest age you can retire without any reduction to your retirement benefit. For TRS Plan 3, this is when you reach age 65. If you have 30 or more years of service and you are age 62, you can also retire with a full benefit. What if you want to retire younger than age 65 and you don’t have 30 years of service?

Early retirement

You can withdraw from your investment account at any time after separating employment. For your employer-funded pension plan, specific rules apply for when you can retire. You can retire as early as age 55 with a reduced benefit if you have at least 10 service credit years.

Early retirement – Joined before May 1, 2013

If you retire before age 65, it’s considered an early retirement. If you have at least 10 years of service credit and are 55 or older, you can choose to retire early, but your benefit will be reduced. There is less of a reduction (in some cases no reduction) if you have 30 or more years of service credit.

If you have 30 or more years of service and you are age 62, you can retire with a full benefit under the 2008 ERF.

How does retiring early affect my monthly benefit?

When you retire early, your monthly benefit amount is reduced to reflect that you will be receiving your pension payments for a longer period of time. The amount of the impact depends on the amount of service credit you have, the date you retire and your age. (See “Early retirement benefit formulas” below.)

If you retire early with 10 – 30 years of service credit, your monthly benefit is reduced by a factor that is based on your average life expectancy. Early retirement factors are subject to change based on State Actuary figures. The reduction is greater than if you retire with at least 30 service credit years.

Early retirement factors

Actuarial early retirement factors, for those with less than 30 years of service, vary by system and plan and are updated at least every six years. See current early retirement factors for Plan 2 members with at least 20 years or Plan 3 members with at least 10 years of service.

- Plan 2: Need at least 20 years of service credit to qualify

- Plan 3: Need at least 10 years of service credit to qualify

Early retirement factors for less than 30 years of service

| Retirement age | Factor |

|---|---|

| 55 | 0.4092 |

| 56 | 0.4450 |

| 57 | 0.4844 |

| 58 | 0.5280 |

| 59 | 0.5760 |

| 60 | 0.6292 |

| 61 | 0.6882 |

| 62 | 0.7538 |

| 63 | 0.8269 |

| 64 | 0.9085 |

Early retirement factors for 30 or more years of service

| Retirement Age | 2008 ERF |

|---|---|

| 55 | 0.80 |

| 56 | 0.83 |

| 57 | 0.86 |

| 58 | 0.89 |

| 59 | 0.92 |

| 60 | 0.95 |

| 61 | 0.98 |

| 62 | 1.00 |

| 63 | 1.00 |

| 64 | 1.00 |

If I retire early, what reductions will apply?

The amount of the reduction to your monthly benefit depends on how much younger than age 65 you are when you retire and the amount of service credit you have. This reduction reflects that you will be receiving your defined benefit for a longer period of time than if you had retired at age 65. Consider how the ERFs are applied in the early-retirement examples shown below.

For more information on early retirement, read Washington Administrative Code 415-02-320.

Plan 3 early-retirement formula

1% x service credit years x Average Final Compensation (AFC) x ERF = monthly benefit

Returning to work could affect your retirement income. See working after retirement.

Early retirement examples

How much difference can early retirement make? That depends on your circumstances, including your wages and age at retirement. Consider the examples below. The administrative factors used in these examples are for illustrative purposes only.

Example 1: Fewer than 30 years

Customer retires Sept. 1, at age 55 with 22 years of service credit.

Their AFC is $3,600. They are retiring early, so using the administrative factor (above table) the monthly benefit is 40.92% of what it would have been at age 65, calculated as follows:

= 1% x 22 years x $3,600 x 40.92%

= 0.01 x 22 x $3,600 x 0.4092

= $324.08 per month

Example 2: 30 or more years

Customer retires April 1, at age 60 with 30 years of service credit using the 2008 ERF.

If they choose to retire under the 2008 ERF, their benefit is reduced by 5% (due to age). The 2008 ERF monthly benefit would be calculated as follows:

= 1% x 30 years x $4,400 x 95%

= 0.01 x 30 x $4,400 x 0.95

= $1,254

Early retirement – Joined on or after May 1, 2013

If you retire before age 65, it’s considered an early retirement. If you have at least 10 years of service credit and are 55 or older, you can choose to retire early, but your benefit will be reduced. There is less of a reduction if you have 30 or more years of service credit.

If you were hired on or after May 1, 2013 and retire early (age 55-64) with 30 years of service credit, your benefit will be reduced by 5% for each year (prorated monthly) before you turn age 65.

How does retiring early affect my monthly benefit?

When you retire early, your monthly benefit amount is reduced to reflect that you will be receiving your pension payments for a longer period of time. The amount of the impact depends on the amount of service credit you have, the date you retire and your age. (See “Early retirement benefit formulas” below.)

If you retire early with 10 – 30 years of service credit, your monthly benefit is reduced by a factor that is based on your average life expectancy. Early retirement factors are subject to change based on State Actuary figures. The reduction is greater than if you retire with at least 30 service credit years.

Early retirement factors

Actuarial early retirement factors, for those with less than 30 years of service, vary by system and plan and are updated at least every six years. See current early retirement factors for Plan 2 members with at least 20 years or Plan 3 members with at least 10 years of service.

- Plan 2: Need at least 20 years of service credit to qualify

- Plan 3: Need at least 10 years of service credit to qualify

Early retirement factors for less than 30 years of service

| Retirement age | Factor |

|---|---|

| 55 | 0.4092 |

| 56 | 0.4450 |

| 57 | 0.4844 |

| 58 | 0.5280 |

| 59 | 0.5760 |

| 60 | 0.6292 |

| 61 | 0.6882 |

| 62 | 0.7538 |

| 63 | 0.8269 |

| 64 | 0.9085 |

Early retirement factors for 30 or more years of service

| Retirement age | 5% ERF |

|---|---|

| 55 | 0.50 |

| 56 | 0.55 |

| 57 | 0.60 |

| 58 | 0.65 |

| 59 | 0.70 |

| 60 | 0.75 |

| 61 | 0.80 |

| 62 | 0.85 |

| 63 | 0.90 |

| 64 | 0.95 |

If I retire early, what reductions will apply?

The amount of the reduction to your monthly benefit depends on how much younger than age 65 you are when you retire and the amount of service credit you have. This reduction reflects that you will be receiving your defined benefit for a longer period of time than if you had retired at age 65. Consider how the ERFs are applied in the early-retirement examples shown below.

For more information on early retirement, read Washington Administrative Code 415-02-320.

Plan 3 early-retirement formula

1% x service credit years x Average Final Compensation (AFC) x ERF = monthly benefit

Returning to work could affect your retirement income. See working after retirement.

Early retirement examples

How much difference can early retirement make? That depends on your circumstances, including your wages and age at retirement. Consider the examples below. The administrative factors used in these examples are for illustrative purposes only.

Example 1: Fewer than 30 years

Customer retires Sept. 1, at age 55 with 22 years of service credit.

Their AFC is $3,600. They are retiring early, so using the administrative factor (above table) the monthly benefit is 40.92% of what it would have been at age 65, calculated as follows:

= 1% x 22 years x $3,600 x 40.92%

= 0.01 x 22 x $3,600 x 0.4092

= $324.08 per month

Example 2: 30 or more years

Customer retires April 1, at age 62 with 30 years of service credit using the 5% ERF.

If they choose to retire under the 5% ERF, their benefit is reduced 5% for each year before age 65. In this case, they are retiring 3 years early, so 5% three times equals a 15% reduction from 100% (so 85%). The 5% ERF monthly benefit would be calculated as follows:

= 1% x 30 years x $4,400 x 85%

= 0.01 x 30 x $4,400 x 0.85

= $1,122

See a live or recorded early retirement webinar.

Considering delaying your retirement? This short delayed retirement video offers some tips and information.

Using sick leave to qualify for retirement

You may use up to 45 days of unused sick leave to help you qualify for retirement. Sick leave not cashed out by your employer may be converted into a maximum of two months of service credit. However, this service credit isn’t used in the calculation of your benefit. It can only be used to qualify for retirement.

How to use sick leave to qualify for retirement

- Request a letter from your employer on their letterhead that states you have the number of sick days available and that you will not be using those days as leave.

- Provide DRS with a copy of this letter for your file.

- We will use those sick leave service credits towards your retirement eligibility, but not in the calculation of your benefit.

- Keep in mind that you will forfeit those days of sick leave if you use them towards service credit.

Once DRS receives your letter, we will add up to two months towards your service credit total, and this can help you reach milestones like:

- Vesting

- Early retirement eligibility

- Reduction of the ERF

For example, let’s say you are age 62 and have 358 months of service credit in TRS Plan 2. If you use sick leave for two months of service credit, you will have 360 months of service credit and that may qualify for retirement under the 2008 early reduction factor (ERF) rules. The 2008 ERF allows some members to retire at age 62 with no reduction for early retirement if they have 30 years (360 months) of service credit. More about early retirement.

Using service credit earned outside Washington state

TRS Plan 2 and Plan 3 customers, you can use service credit earned as an out-of-state teacher to qualify for early retirement or increase your monthly benefit. Two programs are available to you, the Out-of-State Service Credit Program and the Public Education Experience Program. You can participate in either or both. View this short video about out of state service credit.

Out-of-State Service Credit Program

The Out-of-State Service Credit Program can help you qualify to retire early, but you will still have a decreased benefit if you retire before age 65.

Using out-of-state service credit might help you qualify for a smaller reduction for early retirement. However, there is only one way to retire early with an unreduced benefit. You must purchase your out-of-state service credit to reach 30 service credit years (see Public Education Experience Program). Additionally, out-of-state service credit isn’t used in the calculation of your benefit. Your retirement benefit payments would be based only on your Washington state service credit.

This program doesn’t benefit everyone. For example, if you need to use more out-of-state service credit than there are years between your intended early retirement and age 65, using out-of-state service won’t increase your benefit.

To find out if using your out-of-state service credit could benefit you, try this calculator.

To be eligible for this program, your out-of-state service must be earned from a public retirement system that covers teachers. You must also be a vested member of TRS Plan 2 or Plan 3 through DRS.

- For Plan 2, you are vested with five years of service credit

- For Plan 3, you are vested with 10 years of service credit, or with five years of service credit with at least 12 months of it earned after age 44.

You can retire as early as age 55 with a reduced benefit.

- For Plan 2, you need 20 or more years of service credit to qualify for early retirement.

- For Plan 3, you need 10 or more years of service credit to qualify for early retirement.

Additional questions:

Is there a cost to use out-of-state-service credit?

No cost.

Is there a limit to how many years of out-of-state credit I can use?

No limit. See this calculator to find out whether applying the years would be beneficial to you.

What if I have credit in multiple out-of-state systems?

You can use or purchase service credit from multiple out-of-state retirement systems. However, if you do, we can only send one bill. Please mark on the form that you have service in more than one system.

What if I’m already receiving, or eligible to receive, my unreduced out-of-state pension?

If you are collecting your out-of-state pension, or if you are eligible for an unreduced benefit from your out-of-state teachers’ pension system, the following applies. You can still use your out-of-state service credit, but you won’t be able to purchase the service using the Public Education Experience Program.

Public Education Experience Program

If eligible, the Public Education Experience Program gives you an opportunity to make a lump sum payment to increase your monthly benefit in retirement.

- Payment required

- Limit of seven years of service credit

- Service credit must be earned in a federal public retirement system or a state system outside Washington that covers teachers

- Based on both Washington state service credit and purchased service credit

- Increases your service credit, which can give you a higher monthly benefit payment

- Can be used to qualify for early retirement or a smaller benefit reduction

- Must be an active member with at least two years of TRS plan 2 or Plan 3 service credit

How much can I purchase?

You may purchase up to seven years of service credit as long as you have at least that much in out-of-state service credit available. Purchases must be made in whole-month increments. Multiple purchases aren’t allowed. For example, if you buy four years of public education experience now, you won’t be able to make another purchase later.

What type of experience qualifies for service credit purchase?

To qualify for the Public Education Experience Program:

- You must have worked as a teacher in a public school in a different U.S. state or with the U.S. federal government

- You must have been granted service credit for that work in a retirement system

- You can’t already be retired from the out-of-state system (collecting a benefit)

- You can’t be eligible for an unreduced benefit from the out-of-state system

How much does it cost to purchase service credit?

If you choose this program, your Washington state service credit as well as your purchased service credit will be used to calculate your monthly benefit. To estimate the cost, use the Buy Back Calculator for Public Education Experience.

You must pay the amount needed in today’s dollars to pay for the increase in your monthly benefit over your lifetime.

How do I pay?

DRS can accept only full lump sum payments. You can make that payment with either a personal or cashier’s check. In many cases, you can transfer funds from another eligible retirement account to pay your bill as well. DRS can’t accept funds in excess of the cost to make your purchase. To learn more about whether you can make such a transfer, contact your account’s administrator. The Internal Revenue Service classifies DRS as a 401(a) account.

When do I pay?

We must receive your full payment before you retire. After DRS receives your form requesting to buy out-of-state service credit, we will send you a bill to make the purchase. You have 90 days from the bill’s issue date to pay it. If you don’t pay it within that time frame, you will need to request a new bill be sent to you.

Can my employer choose to contribute to the purchase?

Yes. Your current employer can choose to help pay for your service credit purchase. Payments sent in by employers must reference your bill number.

Can I purchase this service credit if I am a substitute?

Yes. If you are working as a substitute teacher and your employer is reporting you as an active substitute, then you are eligible.

What if I quit work and withdraw my contributions?

Half of your purchase amount will be placed in your investment account and is subject to market gains or losses. The remaining half will go into the benefit fund and is non-refundable. Once you separate from employment, you can withdraw funds from your investment account.

How to apply

Contact DRS to request an Application to Use Out-of-State Service Credit. You’ll need your previous retirement system to complete a portion of the form before you submit it to DRS. If approved for the Out-of-State Service Credit Program, we will send you confirmation. If approved for the Public Education Experience Program, we will send you a bill within 30 days.

Related news

Is it better to retire at the beginning of summer or at the end?

When it comes to retirement for teachers and school employees, a few months can have a big impact and substitutes have health care and return-to-work considerations. Read more…

How do you retire?

Plan 3 member, you have two money sources to use toward retirement – an employer funded pension, and an investment account you fund. You must meet service requirements to be eligible for the employer-funded pension. But once you meet those, you are guaranteed a lifetime pension income.

Pension

How to retire with DRS: Pension

When you are within 12 months of retiring, you can start the official retirement process with DRS. First, you request an official benefit estimate. Once you receive the estimate, you complete and submit your application to retire. See this steps to retire with a pension video.

1. Request an official benefit estimate from DRS 3 to 12 months prior to your retirement date. Make this request through your online account or by contacting us. In most cases, we will provide your estimate 5 to 8 weeks before your retirement date. If you haven’t received your requested estimate within 5 weeks of your retirement date, contact us.

Estimates are prioritized by retirement date, which allows DRS to use the most recent information available for you and gives you ample time to submit your retirement application. An official benefit estimate is not the same as the benefit estimator tool available to all customers. To assist your retirement planning any time before or after requesting your official benefit, you can use the benefit estimator tool through your online account.

2. Apply for retirement through your online account. After receiving your official benefit estimate, we recommend completing the application at least 3 to 5 weeks before the date you intend to retire. If you can’t make this timeline, contact us as soon as possible so we can help keep your retirement on track. Members of more than one system will need to complete a paper application.

Estimate your retirement pension income

You can use the benefit estimator tool in your online account to help plan for retirement at any point—while you are still working, and even after you submit an official request to retire. Log into your online account and select the benefit estimator tool to get started.

Plan 3 investment withdrawals

How to withdraw your Plan 3 investments

At any point after you separate from employment, you can begin withdrawing your Plan 3 investment contributions.

To complete your withdrawal online, log into your online account and select your Plan 3 investment account. Under the “More resources” menu, select Request online withdrawal.

Your Plan 3 investment account offers several options for withdrawals. Receive one-time or regular payments in an amount and frequency you choose. Purchase an annuity such as the Plan 3 TAP annuity. Roll your Plan 3 contributions into another eligible employer plan. You can also leave your Plan 3 savings invested for as long as you want even if you separate from Plan 3-covered employment.

You can also contact the DRS record keeper, Voya financial at 888- 327-5596 for assistance with your investment transaction. Or log into your Plan 3 investment account to chat live with a customer service associate. They will help you select the right transaction for your needs.

The amount of time it takes to receive your investment withdrawal depends on where your contributions are invested. See the next section for more information.

What if you separate before retirement?

As a Plan 3 member, you can withdraw your contributions and investment earnings from your investment account at any time after you leave your plan-covered employment. However, if you do, you could reduce an important source of your retirement income.

You made your Plan 3 contributions before the income was taxed. There are tax implications to withdrawing your contributions, so you might want to contact the IRS or a tax advisor before making a decision.

The IRS requires that you begin taking payment of your monthly benefit by the time you are 73, unless you are still employed.

Be sure to keep us up to date on any changes to your name, address or beneficiary. It’s important that you keep your beneficiary designation current. A divorce, marriage or other circumstance might invalidate it.

For more information about your options when separating, see this short career transitions video.

Service credit is cumulative

The service credit you earn toward vesting is cumulative. This means if you separate but later return to public service, you can continue to earn service credit toward your vested status even if you didn’t yet qualify when you separated. For Plan 1 and Plan 2 members, withdrawing your contributions when you separate will set your service credit years to 0.

Plan 3 pension increases

If you have at least 20 years of service credit when you leave employment and do not start to receive your pension, it will increase by approximately 3% for each year you delay receiving it up to age 65 (this is called indexing and is exclusively available to Plan 3).

When do you get paid?

Pension payments

Your pension money will be deposited into your bank account on the last business day of the month, every month, for the rest of your life. The retirement application has a section for your bank information so your funds will be deposited. Once you’ve retired, you can make any updates to your direct deposit through your online account.

Investment withdrawals

The time it takes to begin receiving your investment withdrawals depends on two things:

- Do you have contributions in the WSIB TAP fund?

- Has your employer reported your separation to DRS?

WSIB TAP investment withdrawals

The investment portion (defined contribution) you pay into has investment shares with valuation time periods that vary by the investment program you selected. If you’ve already left service and your employer has electronically uploaded your separation date, the following timelines will apply. It could take an additional 30 days beyond the timeframes given below if your employer hasn’t reported your separation to DRS. Plan 3 members have two investment programs to choose from and you can transfer your contributions from one fund to the other.

Most WSIB Investment Program TAP Fund withdrawals take 6-8 weeks

If your funds were invested in the WSIB TAP fund, you should expect to receive them 6-8 weeks after your request. Your request for payment and separation date from your employer must be received by the third to last business day of the month to meet the cutoff for the monthly pricing the following month, with payment being made at the start of the month after that.

| Request month | TAP value calculated | Payment issued |

|---|---|---|

| January | February | March |

| February | March | April |

| March | April | May |

| April | May | June |

| May | June | July |

| June | July | August |

| July | August | September |

| August | September | October |

| September | October | November |

| October | November | December |

| November | December | January |

| December | January | February |

| Your request and separation must be received by DRS before the third to last business day. If either comes later, use the next month as your request month. | This value is calculated on the 10th business day. | You'll receive payment about a week into the month. |

Example

A January request must be made before the third to last business day. If your separation information or request are submitted to DRS later, consider February as your request month.

For a January request, the TAP value is calculated on the 10th business day of February. You will receive your payment about a week into March.

Why is the WSIB TAP fund calculated monthly?

The fund contains slower moving assets, such as real estate. These assets increase the total diversity of the fund, but it takes more time to assess the value.

Under certain emergency conditions, you can expedite the timing of this withdrawal. Contact the record keeper to find out more 888-327-5596.

All other Plan 3 Investment withdrawals

If you’ve already left service and your employer has provided your separation date, the following timeline will apply. It could take an additional 30 days beyond the timeframes given below if your employer hasn’t reported your separation to DRS.

Most Plan 3 investment withdrawals take 1 to 31 business days For lump-sum payments, investment shares are redeemed daily. If your documents are accepted in good order by 1 pm Pacific Time, your payment is issued the next business day. For scheduled payments, investment shares are redeemed between the first and 27th of every month, and payments are issued on the first or 15th of each month.

How is my withdrawal taxed?

You will pay federal income tax for withdrawals from both your Plan 3 pension and investment accounts. The withdrawal request you complete will include tax information specific to your withdrawal type. Here is some general information about withdrawals.

Investment withdrawals (your contributions)

If you choose a direct rollover, except for a Roth IRA, you are not taxed until you later take payment out of the traditional IRA or the eligible employer plan. Taxes will continue to be deferred.

The IRS requires a 20% tax withholding on any lump-sum withdrawal or if your installment payment plan is expected to last less than 10 years. This means that if you decide to withdraw $10,000 all at once, you will be sent a check for $8,000. The remaining $2,000 will be sent to the IRS. If your installment payments will last longer, you might decide what you would like withheld by completing a form IRS W-4P.

If you receive a payment before you reach age 59½, and you do not roll over your defined contribution funds, you might have to pay an additional tax equal to 10% of the taxable portion of the payment when you file your taxes. Visit the IRS website for more information. If you complete your investment account withdrawal online, you’ll also receive a real-time estimate of your tax withholding. For tax advice, you should consult an accountant, qualified financial advisor, or the Internal Revenue Service.

IRS tax exclusion timing

If contributions to your pension plan were previously taxed, the IRS requires a tax exclusion to the payment you take first: your pension or a withdrawal from your investment contributions. This is sometimes called basis recovery. It prevents you from being taxed again on those contributions. If the exclusion occurs on your pension payment, you will see the amount on your 1099-R in box 5a. It will end once you receive an exclusion equal to the taxed contribution amount. The IRS determines the calculation used for this process.

Pension benefit (employer contributions)

Your monthly pension payments will have standard income tax deducted. We do not deduct any individual state tax, no matter where you live.

For more information about withdrawing from your Plan 3 investment account, contact the DRS record keeper.

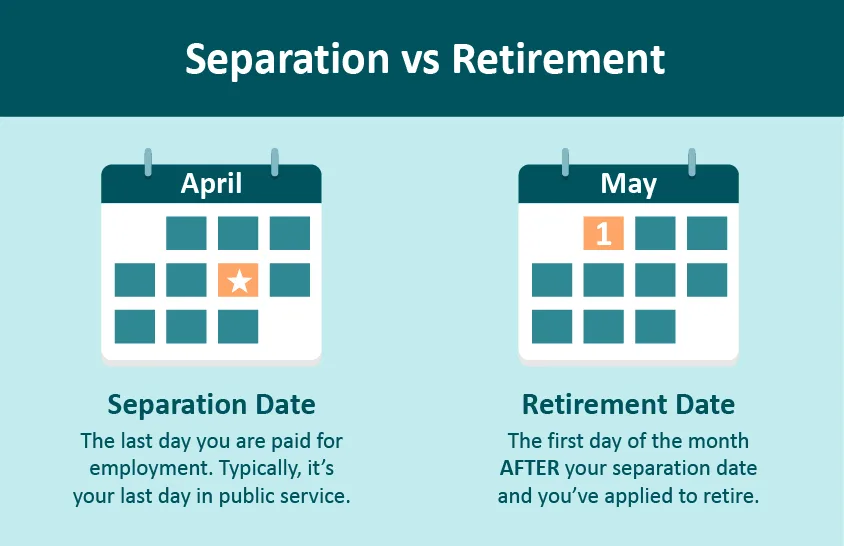

Separation vs retirement

You are retired from DRS when you separate from employment and begin collecting your pension. If you leave public employment, but you are not yet collecting a pension, we consider you separated, but not retired. These instructions assume you are separating and will be collecting your pension (retiring).

See live or recorded retirement planning webinars.

How can you increase your pension amount?

You can increase your pension benefit by increasing your years of service or your income. But when it comes to total retirement income, you have more options.

DCP savings program

The Deferred Compensation Program or DCP is a voluntary savings program you can use to increase your retirement savings. DCP uses many of the same investment options available to Plan 3 members, including investments that are managed for you. With DCP, you control your contribution amount so your savings can grow with you. Saving an additional $100 a month now could mean an extra $100,000 in retirement!

(Example based on 6% annual rate of return over 30 years of contributions.) More about DCP.

Sick leave cashouts

Some employers allow leave cash outs when you separate from employment. These sick leave or vacation cashouts might be a good way to increase your DCP savings when you end your employment. Contact your employer to see what options are available to you.

Plan 3 benefit indexing

Benefit indexing is a form of pension inflation protection you may automatically qualify for when you separate from service. Eligibility for benefit indexing requires you to:

- Be in Plan 3

- Have at least 20 service credit years before you stop working

- Separate before reaching normal retirement and delay receiving your pension benefit

For every month you delay collecting your pension, your benefit amount will be increased by 0.25% (or 3% annually). Benefit indexing stops once you retire or reach your normal retirement age. Once you retire, you’ll instead be eligible to receive an annual maximum 3% COLA.

Benefit indexing example

Francis is a Plan 3 member who is 64 years old, with 20 service years and an average monthly salary of $5,000.

Their Plan 3 benefit calculation is: 1% x 20 years x $5,000. This would provide Francis with $1,000 per month.

In addition to a monthly pension, Francis also has an investment account to draw from in retirement.

Francis also has the option to stop working prior to age 65 but choose not to receive a pension benefit until their first eligible unreduced date of age 65. During that time, their pension will grow. Here are two scenarios of how that could look:

Scenario 1: Stop working at age 64

Start collecting a pension at age 65

The pension benefit increases about 3% in one year (.25 x 12 months = 3)

The pension is $1,030/month

Scenario 2: Stop working at age 65

Start collecting a pension at age 65

The pension benefit calculations is: 1% x 21 years of service x $5,000

The pension is $1,050/month

Annuity options

What’s an annuity?

The annuities offered by Washington state let you convert your savings into guaranteed monthly income for the rest of your life. When you purchase an annuity, you move your money out of market risk and create a steady, predictable income stream.

Annuities are the only investment withdrawal option that ensures you won’t outlive your account balance. Once your annuity is set up, the income amount and terms cannot be changed or canceled.

DRS administers annuities offered by Washington state with investments provided by the Washington State Investment Board.

See a live or recorded annuity option webinar.

Do I have to pay taxes on annuities?

Yes. Like your pension, once you start receiving payments, the money will be taxed as ordinary income.

Each year you’ll receive a statement that shows the taxable amount of your annuity. DRS is required to withhold a certain amount of federal taxes.

- Complete a W-4P form for tax withholding.

- If you don’t submit a W-4P, withholding will default to IRS guidelines, (single with no adjustments).

For more details, review IRS Publication 575 or consult a tax advisor. DRS and the record keeper cannot provide tax advice.

How much will I receive each month?

The amount depends on the purchase price as well as factors like your age and survivorship option. You can estimate your annuity cost and added monthly income by logging into your online account and selecting Purchasing Service or Purchasing Annuity or TAP Annuity Estimator.

When do I purchase?

To purchase the Plan and/or Service Credit annuity, select one or both annuities when you retire online. If you complete a paper retirement application, let DRS know you’re considering an annuity. This will allow us to include an annuity estimate along with your retirement estimate.

To purchase the TAP annuity, contact the DRS record keeper. This annuity can be purchased any time after separating from DRS employment regardless of age.

Compare annuities

| Feature | Plan annuity | Service credit annuity | TAP annuity |

|---|---|---|---|

| Limits | Minimum purchase: PERS, PSERS, SERS: $5,000 TRS: no min LEOFF, WSPRS: $25,000 No maximum for any plan. | Purchase 1-60 months of service credit | Minimum purchase: $25,000 |

| Funding source | Purchase with pretax governmental retirement savings (DCP 457, 403b, TSP). TRS also has a cash option. (See Annuity FAQ) | Purchase with cash or pretax savings (DCP 457, 403b, TSP, IRA, 401k). | Purchase with funds from your Plan 3 investment account. The purchase can take up to 90 days. |

| Eligibility | Available at retirement. | Available at retirement. | Available to Plan 3 members any time after separation. |

| Survivor option | Same as your pension survivor. (WSPRS 1, survivor paid only with Option B.) | Same as your pension survivor. | Can choose a different survivor from pension. |

| Will I receive a COLA? | COLA up to 3% annually. For TRS or PERS 1 member, COLA is optional at retirement. | COLA up to 3% annually. For TRS or PERS 1 member, COLA is optional at retirement. | Guaranteed 3% COLA increase annually. |

| Continues if returning to work | Yes. | Yes, as long as you follow the hourly limits. | Yes. |

| Service credit impact | N/A | Increases monthly benefit, but does not change years of service. | N/A |

| Timing | Can only purchase when applying for retirement. | Can only purchase when applying for retirement. | Can purchase any time after leaving DRS covered employment. |

| The amount paid to you | Based on purchase amount from funding source. | Based on same pension formula as retirement benefit. | Based on purchase amount from funding source. |

| Can be used to qualify for retirement | No. | No. | No. |

| How will I receive this money? | Combined with your pension check. | Combined with your pension check. | You’ll receive a separate deposit from your pension. |

Why do some Plan 3 members choose the TAP Annuity over other DRS annuities?

As a Plan 3 member, you have the option to purchase all 3 annuities. However, many members prefer the TAP annuity because of its guaranteed 3% annual cost of living adjustment (COLA) and flexible time to purchase.

You can purchase the TAP Annuity any time after separating from DRS-covered employment, even if you’re not yet eligible to draw your pension. This is a helpful option for members who separate from service early and want a steady income right away.

Plan vs. Service Credit Annuity — which is better?

Both annuities use the same calculation factors, so the cost and benefit increase are identical. The main difference lies in the funding sources and payment features. You’re not limited to one annuity, you can purchase both.

What happens to my annuity when I die?

If you (and your survivor, if applicable) pass away before the full purchase amount is paid out, your beneficiaries will receive the remaining balance.

Why do plans have different rules?

The rules for each retirement plan are decided by the Washington state legislature and can vary.

TRS plan annuity

This annuity is available to all Teachers’ Retirement System (TRS) members. Unlike purchasing service credit or the Plan 3 TAP annuity, the Teachers’ annuity can be purchased using any of your own funds aside from Plan 3 contributions. With this annuity, your survivor will be the same as the one you selected for your pension payment. If you return to work, this annuity continues.

TRS plan annuity FAQ

When can I purchase?

When you are retiring.

How much does it cost?

Log in to your account and choose “Purchasing Annuity.” Here you can find the monthly increase to your pension for any purchase amount.

Are there limits to the annuity amount I can purchase?

No. There are no minimum or maximum limits.

What funds can I use to purchase the annuity?

You can use any of your own funds, except for any Plan 3 contributions. Funds rolled over from your DCP account must be pretax. If one of your funding sources will be cash or check, the IRS limits the total amount you can pay with this option. The total cash or check must be no more than 100% of your salary in the year of annuity purchase or $72,000 in 2026 (whichever is less).

When does my annuity benefit begin?

Your retirement date or the day after your bill for the annuity is paid in full, whichever comes later.

How often do I receive my annuity benefit?

Monthly.

Can I designate a survivor?

Yes. Your survivor will be the same option you chose for your retirement benefit.

Will I receive a Cost-of-Living Adjustment (COLA)?

Yes. You will receive a COLA up to 3% annually. If you’re a Plan 1 member, a COLA is optional at retirement and your choice will also apply to this annuity purchase.

How do I purchase this annuity?

Request this annuity when you retire online. You can also purchase it when completing a paper retirement application.

Can I cancel the annuity if I change my mind?

In most cases, no. Annuities are fixed income sources. Once you purchase the annuity, you will not have access to the funds you used to make the purchase.

There are two exceptions:

- If you have not completed the annuity purchase, you can still change or cancel the annuity.

- Once you make the purchase, you’ll have 15 days to cancel the transaction. You’ll receive a mailed letter that includes your rescission, or cancel by date.

Will my annuity purchase be refunded when I die?

If you (and your survivor if you selected a survivor option) die before the amount of your annuity purchase has been paid back to you, the difference will be refunded to your beneficiary. This refund option does not apply to the TRS Plan 1 Maximum Option.

What if I return to work?

Your annuity continues.

Purchase service credit annuity

Purchasing additional service credit increases your monthly retirement benefit for the rest of your life. You can purchase between one and 60 months of service credit in whole months. Purchasing service credit will increase your monthly benefit, but it will not increase the years of service posted on your account. The increase to your benefit is calculated using the same formula as your retirement benefit. This additional service credit is available at the time of your retirement only. Also, you cannot use the additional credit to qualify for retirement (it won’t increase your years of service).

Purchase service credit annuity FAQ

When can I purchase?

When you are retiring.

Are there limits to the amount of service credit I can purchase?

Minimum: One month; Maximum: 60 months.

How much does it cost?

Log in to your account and choose “Purchasing Service.” Here you can find the estimated cost and income increase per month you purchase.

What funds can I use to purchase service credit?

You can use any funds except for Plan 3 contributions. Funds rolled over from your DCP account must be pretax.

When does my annuity benefit begin?

After you have made payment in full.

How often do I receive the benefit?

Monthly.

Can I designate a survivor?

Yes. Your survivor will be the same option you chose for your retirement benefit.

Will I receive a Cost-of-Living Adjustment (COLA)?

Yes. You will receive a COLA up to 3% annually. If you’re a TRS Plan 1 or PERS Plan 1 member, a COLA is an optional choice at retirement.

Can I cancel the annuity if I change my mind?

No. Annuities are fixed income sources. Once you purchase the annuity, you will not have access to the funds you used to make the purchase. If you have not completed the annuity purchase, you can still change or cancel the annuity.

How do I purchase service credit?

Request this annuity when you retire online. You can also purchase it when completing a paper retirement application.

Will my annuity purchase be refunded when I die?

Yes. If you (and your survivor if you selected a survivor option) die before the amount of your purchase has been paid back to you, the difference will be refunded to your beneficiary. For TRS Plan 1, this refund does not apply if you selected the Maximum Option.

What if I return to work?

The return to work rules for service credit are the same as your retirement benefit. If you return to work for a DRS-covered employer, your annuity will stop if you return to retirement system membership or if you exceed allowable hours as a retiree (867 per year). If you do not return to a DRS-covered employer, your annuity will continue.

When will my benefit increase be effective?

The increase in your benefit will be effective the day after the department receives your full payment.

Plan 3 TAP Annuity

Plan 3 members can use their plan contributions to purchase the Total Allocation Portfolio (TAP) Annuity. With the TAP Annuity, you are not limited to the survivor options you chose for your pension retirement. You can choose another survivor. You can also purchase the TAP Annuity any time after you separate from DRS-covered employment.

It can take 45 to 90 days to receive your first TAP Annuity payment. See the payment section below for a timeline of the purchase process. For information about the status of your annuity purchase, contact the DRS record keeper.

Plan 3 TAP Annuity FAQ

When can I purchase?

When DRS receives your separation date, or any time after.

Are there limits to the annuity amount I can purchase?

Minimum: $25,000; Maximum: Your total Plan 3 investment account balance.

How much does it cost?

Use the TAP Annuity Estimator calculator or contact the Plan 3 record keeper.

What funds can I use to purchase the annuity?

Contributions from your Plan 3 investment account. To purchase the annuity using funds from both your WSIB and Self-Directed investment programs, you’ll need to transfer the funds to either the WSIB program or the Self-Directed Investment Program first.

How often do I receive my annuity benefit?

Monthly.

Can I designate a survivor?

Yes.

Can I cancel the annuity if I change my mind?

In most cases, no. Annuities are fixed income sources. Once you purchase the annuity, you will not have access to the funds you used to make the purchase.

There are two exceptions:

- If you have not completed the annuity purchase, you can still change or cancel the annuity.

- Once you make the purchase, you’ll have 15 days to cancel the transaction. You’ll receive a mailed letter that includes your rescission, or cancel by date.

How do I purchase an annuity?

Complete the purchase online or call the Plan 3 record keeper at 888-327-5596 for assistance.

Will I receive a Cost-of-Living Adjustment (COLA)?

Yes. Your TAP annuity will receive an automatic COLA of 3% annually. This COLA is applied on the anniversary of the annuity.

Will my annuity purchase be refunded when I die?

If you (and your survivor if you selected a survivor option) die before the amount of your annuity purchase has been paid back to you, the difference will be refunded to your beneficiary.

What if I return to work?

Your annuity continues.

Can I buy more than one TAP Annuity?

No. You can buy only one TAP Annuity.

What else should I know?

You don’t need to be separated to move money into the TAP investment program, only to purchase the TAP Annuity.

You can purchase the TAP Annuity and start receiving monthly payments at any age.

You can purchase the TAP Annuity anytime you qualify to receive a distribution—between employment opportunities, at retirement or any time after retirement.

You can only purchase the TAP Annuity one time per retirement system membership (one each for PERS, SERS or TRS accounts).

The 3% Cost-of-Living increase (COLA) will be added to your payment each year on the anniversary of your annuity purchase.

How can I find out more?

Contact the Plan 3 record keeper for assistance.

How can I get assistance with my account once I purchase the TAP annuity?

To update your withholding, beneficiary information, direct deposit or for other inquiries, TAP annuitants can contact the DRS record keeper, Voya Financial for assistance.

When do I receive my first TAP Annuity payment?

How long does it take?

About two months. Your first payment could take anywhere from 45 to 90 days. The most common timeline is about two months. The timeline includes DRS receiving your request and a separation date from your employer. Your employer usually sends your separation date with your final contributions to DRS after you receive your final paycheck—that could take up to 45 days depending on your employer’s reporting process.

Why does it take this long?

The price for the WSIB TAP fund is calculated each month, after the end of the month. When you request to purchase a TAP Annuity, it can take two or more months to know the value and have the final reporting from your employer.

Example: TAP Purchase timeline

1 Request and separation

July 9 – The customer separates employment and completes TAP Annuity purchase request.

July 26 – DRS receives a separation date from the employer.

2 Price and purchase

Aug. 13 – The TAP valuation from July is applied to calculate the value of the TAP shares.

Aug. 30 – An annuity contract is created on the 2nd to last business day of the month and sent to the customer. They will have 15 days to rescind the contract.

3 Contract and payment

Sept. 3-10 – The first TAP Annuity payment is issued to the customer. Depending on the form of payment (paper check or direct deposit), the customer receives the payment between the third and tenth of September, and will receive payments on or around the same day each month.

Why is my separation date important?

If the DRS record keeper has not received completed paperwork from the customer or the employer has not sent the separation date by the third to last business day of the month, it could add an additional month to the purchase timeline. DRS cannot distribute the funds until the employer has notified DRS of the separation of the customer, which will not take place until sometime after the customer has received their last paycheck from the employer. For TRS and SERS members who separate or retire in the summer, this means that annuity payments will not start before September and likely won’t begin until November.

What is the fastest way to purchase the TAP Annuity?

There are a few actions you can take to ensure your annuity purchase goes smoothly.

Transfer your funds into the WSIB TAP investment program prior to making your TAP Annuity purchase. Transfer your funds online or contact the record keeper to start the transfer so you don’t have to wait until you stop working.

Complete your TAP Annuity purchase request online through your Plan 3 account. Ensure that the DRS record keeper has all necessary information before the third to last business day of the month.

Check in with your payroll office to know when they will be sending your separation date to DRS. If DRS receives this information after the third to last business day of the month, it will delay the purchase cycle another month.

Why is the WSIB TAP fund calculated monthly?

The fund contains slower moving assets, such as real estate. These assets increase the total diversity of the fund, but it takes more time to assess the value.

See a live or recorded annuity option webinar.

Investments

Plan 3 customers have investment accounts you fund with a percentage of your income.

We offer two types of funds: One-step or build and monitor. All funds are managed by the Washington State Investment Board.

One-step: These investments are automatically adjusted for you based on your age. The One-Step Investing approach includes Retirement Strategy Funds, also called age-based or target date funds. Because most customers choose one-step investing, this is also the default investment type for customers who do not select investments.

Plan 3 also includes a fund called the WSIB TAP or Total Allocation Portfolio. This is also a one-step investment program. However, this fund is not adjusted based on your age, but is managed in the same way the state pension fund is invested. If you select this option, all your new contributions will be invested in this fund.

Build and monitor: This is the DIY approach to investing where you choose from a selection of investments and create your own mix from a list of funds.

Investments and fees

Select the funds below to view their fact sheets. Funds for each table are listed in order of risk (lowest to highest). View the latest performance for all funds through your online account. The management fees associated with each fund are included here. These costs are in addition to the administrative fees detailed in the table lower in this section.

Retirement Strategy Funds (Fees as of July 2025)

Build and monitor funds (Fees as of July 2025)

| Funds | Manager fee |

|---|---|

| Short-Term Investment Fund | 0.081% |

| Washington State Bond Fund | 0.001% |

| Socially Responsible Equity Investment | 0.42% |

| US Large Cap Equity Index Fund | 0.001% |

| Global Equity Index Fund | 0.035% |

| US Small Cap Value Equity Index Fund | 0.018% |

| Emerging Market Equity Index Fund | 0.09% |

WSIB Investment Program

| Funds | Manager fee |

|---|---|

| Total Allocation Portfolio (TAP) | 0.5162% |

Funds are classified into two investment programs: Self-Directed and WSIB. Only the WSIB TAP fund is part of the WSIB investment program. The classifications are important for Plan 3 members when it comes to withdrawing your funds. Self-Directed fund values are calculated daily, whereas the WSIB TAP fund is calculated monthly. Plan 3 customers can transfer balances between the two investment programs. See when do you get paid for more information about timelines.

Investment performance

Compare the most recent performance for your Plan 3 investments through your online account. You can also access a quarterly overview of fund performance in the table links that follow.

Administrative fees (as of July 2025)

| Fee Type | Percentage |

|---|---|

| WSIB fee | 0.0167% |

| Recordkeeping fee | 0.0740% |

Investments have two types of costs. The management cost for the individual investment and the administrative costs applied to all plan investments. This table includes the administrative costs in addition to your fund fee in the previous tables. Find out more about investment costs in this video or in the investment faq section.

Managing your investments

Make investment changes through your online account. Change your fund selections anytime during or after your employment. You can also contact the record keeper for assistance. To change the investment program for future contributions, complete this form and give it to your employer.

Trading restrictions:

To safeguard customers against the effects of excessive trading, DRS has established trading restrictions that regulate how frequently you can change investments.

If you are transferring more than $1,000 out of a fund, you are required to wait 30 calendar days before transferring money back into that same fund. The 30-day window is based on the last time you made a transfer out of the fund. The restriction will not affect your regular contribution or the ability to leave state service and withdraw your money. Transfers of $1,000 or less are not impacted by the trading restrictions.

DRS periodically reviews trade data to identify excessive trading. If existing restrictions are not sufficiently addressing excessive trade practices, DRS might take additional action. DRS reserves the right to establish or revise restrictions to comply with federal or state regulations, or as circumstances indicate.

In addition to the trading restrictions described above, DRS will also comply with restrictions put in place by our fund managers.

Note: Excessive trading (also referred to as “market timing”) involves transferring significant amounts of money and/or making frequent trades between investment options. This practice requires more cash on hand to honor the frequent trades and transfers. Because the excess cash is used to cover potential transfers instead of being invested, long-term returns can be lowered for other participants. Excessive trading can also increase fund management costs.

Investment FAQ

Can DRS tell me what to invest in?

No. While DRS and the Plan 3 record keeper can provide information about investments, we cannot offer investment advice. Find out more about each fund by reviewing the fact sheet linked to the fund name in the investments and fees section. These fact sheets are prepared by the fund managers and contain information about performance, asset mixes and the goals of the fund. If you aren’t sure which investment approach might be right for you, talk with your financial advisor.

How do I choose a one-step Retirement Strategy Fund?

Take your birth year and add the age you expect to retire. That gives you a target year. Then you pick the fund with the date closest to that year.

Example: If you were born in 1993 and want to retire at 65 → 1993 + 65 = 2058 → pick the 2060 fund.

How do I withdraw my Plan 3 investments?

At any point after you separate from employment, you can begin withdrawing your Plan 3 investment contributions. To complete your withdrawal online, log into your online account and select your Plan 3 investment account. Under the “More resources” menu, select Request online withdrawal. Your Plan 3 investment account offers several options for withdrawals.

Are there fees with Plan 3 investments?

Yes, but they’re pretty low. Even though investment fees are often small (fractions of a percent), they do add up over time. It’s good to know the cost differences when you compare investment options as well. Plan 3 has two types of fees:

1. Administrative Fees

These cover fund costs like recordkeeping, communications, customer service, and oversight by the Washington State Investment Board (WSIB).

- The total WSIB and recordkeeping admin cost for Plan 3 is 0.0907% per year.

- It’s built into the share price, so you won’t see it listed on your statement.

- This fee is reviewed annually and may change each July.

2. Management Fees

These are what you pay the professionals who manage the funds. Review the management fees within the fund fact sheets linked in the investments and fees section.

You can switch your investment choices at any time, and it’s smart to check the management fee before making changes.

The amount varies depending on the fund you choose.

Like admin fees, these are included in the share price and not shown on your statement.

Example of fees applied to a $10,000 balance

Let’s say you have $10,000 in the 2035 Retirement Strategy Fund. Here’s how the annual fee breaks down:

• 0.21% (Fund manager fee)

• 0.0167% (WSIB admin fee)

• 0.0740% (Recordkeeping admin fee)

• Total: 0.3007%

So, $10,000 x 0.003007 = $30.07 per year in fees.

How do I move money between the WSIB TAP and the Self-Directed funds?

You can move existing investment account funds to or from Self-Directed or WSIB. To move all or a portion of these funds, contact the DRS record keeper. The TAP Fund is valued only once a month and the transfer of funds can take up to 45-90 days to complete.

To change your future payroll contributions to or from Self-Directed or WSIB, complete this form and give it to your employer.

What is fund risk, performance and diversification?

Here’s the quick rundown:

Risk: All investments carry some risk. Generally, younger folks can handle more risk (more growth potential), while people nearing retirement often choose safer options. How much risk you take is really up to you.

Performance: Past returns aren’t a promise for future ones, but they can show how the fund tends to behave.

Diversification means spreading your money around, like not putting all your eggs in one basket. That way, if one investment drops, others might balance it out.

- If you go with a Retirement Strategy Fund (the “One-Step” option), it’s already diversified and will adjust automatically as you get closer to retirement.

- If you want more control (the “Build and Monitor” route), you can mix and match between different funds.

Can I invest in funds that aren’t listed here?

No. DRS does not offer a brokerage account option, and you must select from the lineup available. Each fund typically includes a mix of investments, such as stocks from various companies. You can review the fact sheets in the available investments section to see a summary of what’s included in each option.

All investment options for DRS plans are selected by the Washington State Investment Board (WSIB). If there are funds you would like to see, you can submit public comment to WSIB.

Where can I get more information about investing?

Investment fee comparison

Compare how investment fees can impact your account using this calculator.

Investment basics webinar

This DRS recorded webinar explores the investment options available to DCP and Plan 3 customers.

Financial Literacy and Education Commission

MyMoney.gov promotes financial literacy and education. Find out how to plan for life events with financial impacts, such as birth or adoption of a child, home ownership or retirement.

U.S. Securities and Exchange Commission (SEC)

The SEC provides investment regulation and education.

Washington State Department of Financial Institutions (DFI)

DFI provides regulatory oversight for our state’s financial service providers.

Washington State Investment Board (WSIB)

WSIB closely monitors the performance of all DCP investment options.

Required minimum distribution

What is a required minimum distribution (RMD)?

If you are a Plan 3 customer who is separated or retired, you must withdraw a minimum amount from your retirement investment accounts every year starting when you reach age 73. This minimum distribution of funds is required by federal income tax regulations. DRS calculates and pays out the minimum amount to you each year. This is to help you avoid the 25% tax penalty the IRS can impose if the minimum is not withdrawn.

The payments are automatically distributed to you, so no actions are needed for you to meet the requirements. But you can also choose to make adjustments to the distribution, such as the frequency of payments. Here is the form you need:

If you have investment funds in both the Self-Directed and the WSIB programs, your minimum payment will be withdrawn from your WSIB investment program account first. By completing the Plan 3 RMD form yourself, you can choose to have the money withdrawn differently.

Note: The SECURE Act has raised the RMD age from 70 ½ to 73 for most retirees. Age 73 applies to any member who has separated from service and was born on or after January 1, 1951. If you were born before July 1, 1949, then you must commence your retirement benefit at the later of age 70 ½ or when you separate from service. If you were born after June 30, 1949 but before January 1, 1951, then you must commence your retirement benefit at the later of age 72 or when you separate from service.

How is the minimum payment calculated?

You can calculate your required minimum distribution by taking the previous year’s Dec. 31 investment account balance and dividing it by the IRS distribution period based on your age. If you are a member of Plan 3 and DCP, you have two investment accounts that are subject to minimum distribution requirements and you calculate these separately.

To calculate your own RMD withdrawal, use the table linked below. Find your age in the table. The distribution period is the number you divide your total investment account balance by to get the required minimum amount.

IRS distribution period for your age

See the IRS distribution period for your age.

This table applies to you if your status is:

- Unmarried

- Married with spouse who is not more than 10 years younger

- Married with spouse who is not the sole beneficiary of your account

When is it due?

DRS must issue your minimum payment by Dec. 31 to meet IRS requirements. You’ll usually receive your payment earlier in December. DRS will send you 1-2 reminder letters in the year you turn age 73 so you’ll know the RMD is coming. In the years after age 73, these payments will be automatic. You can change the frequency and amount of payment anytime by completing a Plan 3 withdrawal. Your withdrawal amount must at least meet the required annual minimum.

How do the requirements apply to a surviving spouse or beneficiary?

If the original account holder dies, the required minimum distribution is still required for beneficiaries of the account. Here’s how these requirements work:

A spousal beneficiary will be required to continue receiving RMD payments if the account owner had already met the required age. If the account owner had not reached the required age prior to death, the spousal beneficiary will be required to start their RMD payments in the year in which the account owner would have turned age 73.

For non-spousal beneficiaries, the RMD is calculated based on the beneficiary’s life expectancy in the calendar year immediately following the account owner’s date of death. DRS will process an RMD payment if the account owner had turned age 73 or older. If the account also has rollover requests, the RMD will be processed before these.

What if I’m still employed?

If you are still employed by the same DRS-covered employer, the minimum distribution requirement does not apply to you. If you separate from your Plan 3 covered employment and you are age 73 or older, the RMD will apply.

More information

To find out more, contact the DRS record keeper at 888-327-5596 or visit the RMD section of the IRS website.

This information about required minimum distributions is a summary. For a complete description of RMD rules and information, see Required Minimum Distributions on the IRS website. If a conflict exists between the information on this page and what is contained in current law, the law governs. Please talk with your financial advisor if you have questions about taxes on your investment funds. DRS team members aren’t able to give tax advice

Life events that can affect your pension

Death

Death of a retired member

Please contact DRS as soon as possible. If the retiree chose a survivor benefit, we must update the account for payments to continue. If the retiree did not select a survivor option, we need to stop monthly benefits to avoid an overpayment.

When you contact us, please be ready to provide the deceased retiree’s:

- Full name

- Social Security number

- Date of death

We’ll also ask who is handling the affairs for the estate.

Report a death to DRS

Online: Report the death online.

Phone: 360-664-7081, Option 1

Email: drs.moddnd@drs.wa.gov – Please provide only the last 4 digits of the deceased’s SSN

Mailed form: Print and mail this death reporting form to DRS.

Death of an active or not yet retired member

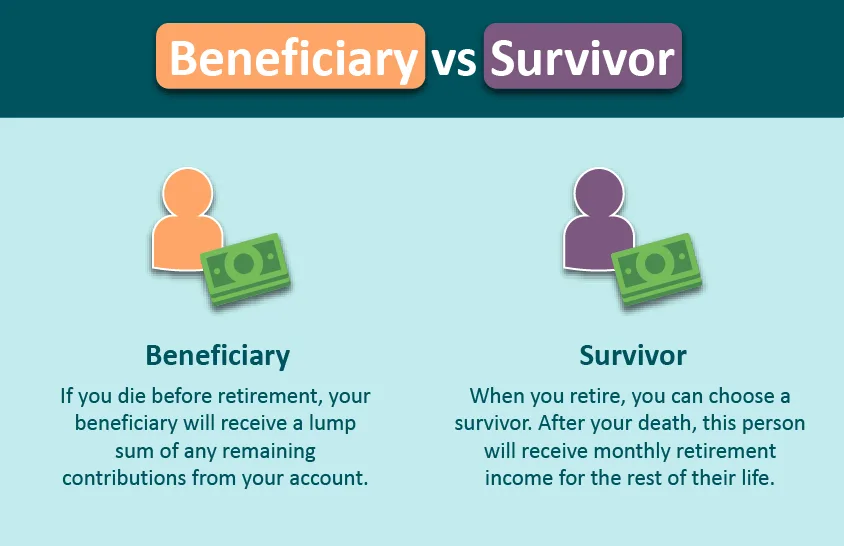

If a member passes before separating from their Washington public service position, their contribution balance plus interest will be paid out to their beneficiaries.

However, if they worked for at least ten years, a surviving spouse or partner could have the option to inherit the account as pension payments. This option is available if the member worked at least ten years (or reached vested status in Plan 3). Contact DRS for information about eligibility and retirement timing.

When you contact us, please be ready to provide the deceased member’s full name, Social Security number and date of death. Also tell us if the death may be work-related.

Death of a beneficiary or survivor

If you are an active member, you can update your beneficiary designation at any time by logging into your online account.

If your named survivor dies after you retire, you can have your pension benefit changed to the single-life option with no survivor reduction. You will need to report the death to DRS. This provision applies to all DRS plans except for LEOFF and WSPRS Plan 1.

More resources

Information for beneficiaries, claimants and survivors

Death & Disability Benefits Webinars (PERS SERS TRS & LEOFF 2)

Disability

If you become totally incapacitated and leave your job as a result, you might be eligible for a disability retirement benefit. The disability retirement was originally created for customers who wouldn’t otherwise be eligible to start receiving a retirement benefit. Even if you have not yet reached the minimum age for retirement, or you are not yet vested in your plan, you can still apply for a disability retirement.

Do you already qualify for retirement?

If you are vested in your plan and qualify to retire, there is no financial benefit to taking disability vs retirement, even for early retirement. The income you receive for either retirement uses the same calculations. Early or full retirement is also a much faster process than disability retirement.

How to apply for a disability retirement?

Call DRS and request an official estimate for a disability retirement. It takes about 3-4 weeks for DRS to calculate your benefit. Then we will mail you a packet with the estimate and a three-part form. You, your employer and your doctor will need to complete all three forms in the packet.

Once DRS receives the completed application and all supporting documentation, it usually takes about four to six weeks to determine your eligibility for a disability retirement.

The full application process averages 4-5 months from the time you request the estimate, but the timing can vary. Providing all requested documentation along with a complete application can help reduce the wait time.

If the disability retirement is approved, your retirement date would be the first of the month after your separation date. DRS would issue your monthly benefit payments on the last business day of the following month and every month after.

Returning to public service

Returning

If you leave your position, withdraw your contributions and later return to TRS work, you can restore your Plan 3 contributions at any time unless you waived your pension benefit.

A dual member, or someone who belongs to more than one retirement system, might be able to restore service credit earned in a retirement system other than TRS. Each time you become a dual member, you’ll have 24 months to restore service credit earned in a previous retirement system. It might still be possible to purchase service credit after the deadline has passed. However, the cost in that case is considerably higher.

To explore financial projections and comparisons of your estimated retirement benefits, try using the Plan Choice Calculator.

Retired? See working after retirement.

Missing or withdrawn service credit

Service credit is the time used to calculate your pension retirement income. Sometimes customers notice their service credit doesn’t match their seniority date—these times do not always match. Often, the difference is because of missing or withdrawn service credit. You may be eligible to purchase some or all of the missing credit. Here is what you need to know about the process.

How do I check my service credit?

View your complete service credit history through your online account. It is a good practice to check your service credit every few years to be sure it matches your expectations.

Contact DRS for a cost estimate

You will need to contact DRS to request a cost for restoring your credit. We are not able to provide an estimate when you call. Similar to a retirement benefit estimate, this cost must be calculated by DRS and may require information from your employer.

You’ll need this information

The following preparation can expedite your request:

Provide the dates for the missing service. Find your service credit history in your online account.

Let us know if there is a gap in your service credit or if you withdrew from your account.

- If there is a gap in your service credit, do you know why? Were there any special circumstances around your employment at the time? Some common events for missing credit include: authorized leave of absence, childbirth, substitute teaching, temporary duty disability, or injury.

- If you withdrew from your account, when did you pull out the contributions?

How do I pay?