Glossary

Account balance

The total amount of your member contributions plus interest. This total can include tax-deferred contributions, after-tax contributions, post-30-year contributions, extra contributions and interest.

Active member

Customers who are employed and contributing to their DRS retirement account. (See also Inactive member.)

Annuity

An additional benefit option you purchase. Annuities usually provide you with lifetime payments, but you can also select annuities that last a certain number of years (term certain). See Purchase an Annuity for more information.

Asset

Any tangible or intangible item that has value in an exchange. A bank account, a home or shares of stock are all examples of assets.

Asset classes are investments that have similar characteristics. The three main asset classes are stocks, bonds and cash.

- Stock: An instrument that signifies an ownership position (called equity) in a corporation, and a claim on its proportional share in the corporation’s assets and profits. Most stock also provides voting rights, which give shareholders a proportional vote in certain corporate decisions, such as the election of corporate directors.

- Bond: A debt security, similar to an IOU. When you buy a bond, you are lending money to an issuer. In return for the loan, the issuer promises to pay you a specified rate of interest during the life of the bond and to repay the principal when it “matures,” or comes due.

- Cash equivalents: Short-term investments that are readily convertible into cash, such as money market holdings, short-term government bonds or Treasury bills, marketable securities and commercial paper.

Average Final Compensation (AFC) period

The monthly average of your highest-paid service credit months. The AFC period for Plan 1 is 24 consecutive months. The AFC period for Plan 2 and Plan 3 is 60 consecutive months.

Benchmark

The performance objective standard represented by a model portfolio used to define the return against which another portfolio is to be evaluated.

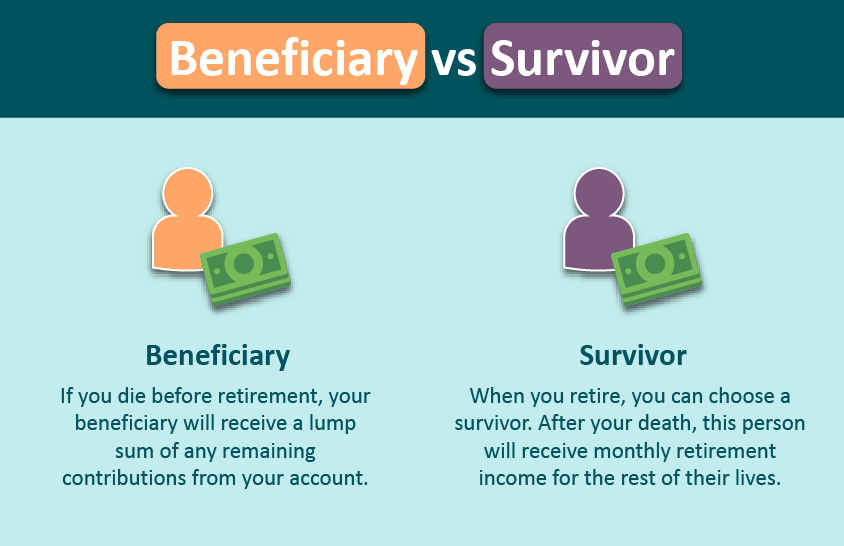

Beneficiary

The person(s), estate, organization or trust you have designated to receive any benefits payable upon your death. Your beneficiary will receive payment if you die. Be sure to keep your beneficiary information up to date with DRS.

Benefit

Also called a pension, this is the monthly income you receive when you retire.

Benefit Option

The option you select at retirement to indicate whether to provide payment to a survivor after your death. Option 1 does not provide a monthly payment to a survivor after your death. All other options do provide a continuing payment to a survivor. Once you retire, you can change your option only under limited circumstances. This selection is permanent, except as indicated in the How Your Benefit Option Can Change section of the estimate statement. See your plan guide for more information. This survivor options video provides a 2 minute overview of your benefits.

Cost-of-living adjustment (COLA)

A COLA is an adjustment to your monthly benefit after you retire. The type of COLA you are eligible for depends on your retirement system and plan. More about COLAs.

- Plan 1 You may select the optional COLA, which is described in the estimate.

- Plans 2 and 3 On July 1 of every year following your first full year of retirement, your monthly benefit will be adjusted to reflect the percentage change in the Seattle Consumer Price Index — to a maximum of 3% per year.

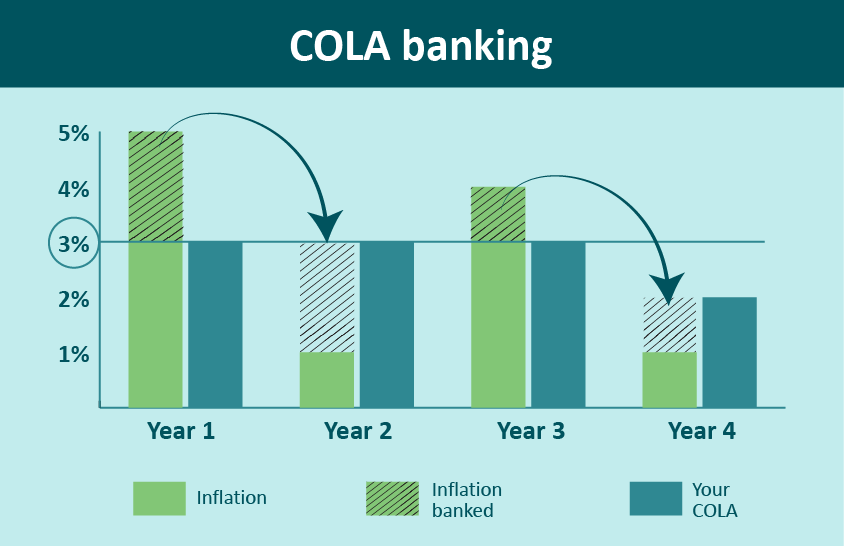

COLA banking

The maximum annual COLA you can receive for most DRS plans is 3%. If inflation that year is above 3%, the additional amount is applied to future adjustments (this is called COLA banking). Any year inflation is lower than 3%, the COLA can pull from banked percentages in prior years.

This happens automatically and the adjustment is made for you. You may receive a different adjustment each year, depending on the amount available in your COLA bank.

Deductions

Any amount deducted from your gross benefit. Deductions can be taken for federal income taxes, health insurance, supplemental life benefit, auto insurance, union dues or other items.

Deferred Compensation Program (DCP)

A supplemental retirement savings program offered by Washington state. DCP is a pretax 457(b) program. More about DCP.

Defined benefit

Also called a pension plan at DRS, this is a retirement plan in which your benefit is based on a set formula rather than an account balance. The formula provides a retirement benefit based on your years of service and the average of your final salary.

Defined contribution

A Plan 3 member investment account that consists solely of the money you contributed and any income, expenses, gains or losses applied to your account.

Diversification

Diversification is a strategy that can be neatly summed up as “Don’t put all your eggs in one basket.” The strategy involves spreading your money among various investments in the hope that if one loses money, the others will make up for those losses. Dividing investments among different kinds of assets, such as stocks and bonds, with different risks and returns, can minimize the potential harm from any one asset.

Domestic partner

Qualified domestic partners have the same survivor and death benefits as married spouses. However, differences could occur in how taxes are handled at the federal level. In a qualified domestic partnership, both individuals have met the state’s legal requirements and registered their partnership with the Secretary of State’s Office or another jurisdiction. Contact the Secretary of State’s Office if you have questions about the requirements.

Dual member

You are a dual member if you have established membership in more than one Washington state retirement system, including First Class City Retirement Systems for Seattle, Spokane and Tacoma. We also refer to this as multiple plans.

Early retirement

In most cases, if you retire before you turn age 65, your monthly benefit is reduced to reflect the fact that you will receive it over a longer period of time. The amount of the reduction depends on how much younger than age 65 you are when you retire and the amount of service credit you have. Some systems allow a full retirement benefit at an earlier age. See your plan.

Early retirement reduction factor

Also called an ERF, this is a reduction factor used in the benefit calculation when you retire before meeting requirements for a normal retirement. The Office of the State Actuary provides these factors. See WAC 415-02-320 for more information.

Final Average Salary (FAS)

A system for averaging LEOFF member salaries.

- LEOFF 1 The FAS is determined as follows:

- If you held the same position or rank for at least 12 months preceding your retirement, your FAS is the basic salary for that position or rank at the time you retire. (If you previously held a higher-ranking position for at least 12 months, contact LEOFF.)

- If you didn’t hold the same position or rank for at least 12 months preceding your retirement, your FAS is the monthly average of your highest-paid 24 consecutive months within your last 10 years of credited service.

- If you are a vested member who separated from employment before becoming eligible to retire, your FAS is your basic salary at the time you left service.

- LEOFF 2 The monthly average of your highest-paid service credit months. The FAS period for LEOFF Plan 2 is 60 consecutive months.

Full retirement

Also called Normal Retirement, this is a retirement benefit that is not reduced because you retired from public service at the normal minimum retirement age. For most members, this is age 65. For some systems, like PSERS, full retirement age is younger than 65.

Gross benefit amount

The total amount of your retirement benefit payment before any deductions have been taken.

Inactive member

Customers who have contributed to their account in the past and are not currently employed in a DRS retirement-eligible position. This can include retired customers. (See also Active member.)

Investments

Plan 3 and DCP customers pay a portion of income to accounts that are invested in the stock market. For more about investment terms, see the Plan 3 or DCP investment pages.

LEOFF

Law Enforcement Officers’ and Fire Fighters’ Retirement System – One of the DRS retirement systems. See all plans.

Net benefit amount

The total amount of your retirement benefit payment after all deductions have been taken.

Pension

Your monthly retirement benefit.

PERS

Public Employees’ Retirement System – One of the DRS retirement systems. See all plans.

Post-30-year contributions

Plan 1 members with 30 or more years of service credit can make a one-time, permanent election to have any contributions made after the date of election refunded to them at retirement. Such contributions are deposited in a separate account and earn 7.5% interest.

PSERS

Public Safety Employees’ Retirement System – One of the DRS retirement systems. See all plans.

RCW

Revised Code of Washington

Record keeper

The DRS record keeper is a third party vendor who maintains the records for Plan 3, DCP and JRA customer investment accounts and assists customers with transactions related to these accounts. More record keeper information.

Reduced benefit

A benefit that has been reduced based on factors the Office of the State Actuary provides.

Rescission period

Length of time you can alter or cancel an annuity.

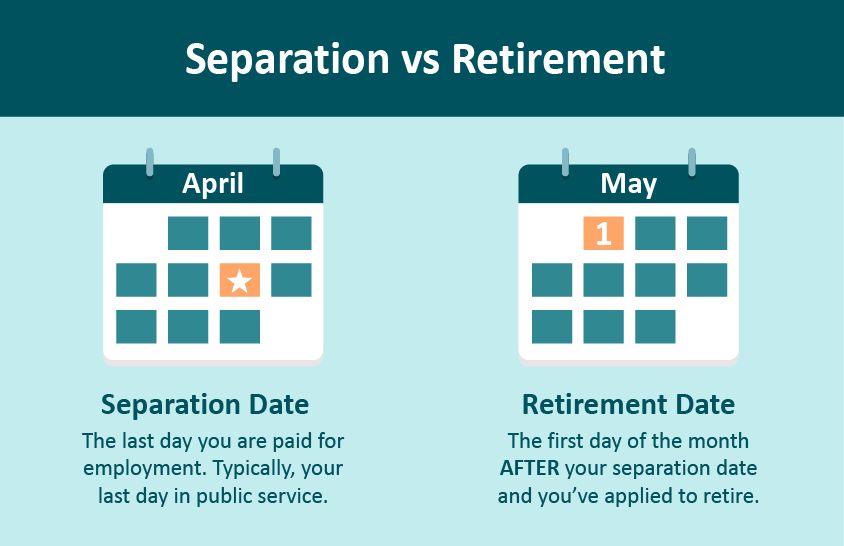

Retirement date

For most plans, after you apply for a retirement benefit, your effective retirement date is the first of the month following your date of separation. For more information, see your plan page.

Retirement eligibility

You meet the age and service requirements for your system and plan. For more information, see your plan page.

Retirement Strategy Fund

Also called a target date fund, this is a diversified mutual fund that automatically shifts toward a more conservative mix of investments as it approaches a particular year in the future, known as its target date. The investor picks the fund with the date closest to the date they want to begin withdrawing their contributions. The managers of the fund then make all decisions about asset allocation, diversification and rebalancing.

Return to work

Working for a DRS-covered employer while receiving a retirement benefit. Returning to work could impact your benefit. See the returning to work section of your plan for more information.

Risk

The degree of uncertainty about the rate of return on an asset and the potential harm that could arise when financial returns are not what the investor expected. In general, as investment risks rise, investors seek higher returns to compensate them for taking on such risks.

Self-Directed Investment Program

One of two investment program types available to Plan 3 members of PERS, SERS and TRS. If your investment contributions are not in the WSIB fund, they are Self-Directed. You can transfer funds between the two programs.

Separating from service

You complete the necessary actions to leave employment. For example, you return any employer-issued items, your computer access is shut off and your employment in the payroll system is ended.

Separation date

The date you end employment with a DRS-covered employer. This is different from your Retirement Date.

SERS

School Employees’ Retirement System – One of the DRS retirement systems. See all plans.

Service credit

The credit you receive each month for working in a position covered by one of the state retirement systems. You can receive one-quarter, one-half (Plans 2 and 3 only) or one month of service credit for each month of employment, based on the number of hours you work. Service credit is used to determine your eligibility for retirement and your benefit amount. More about service credit.

Service credit years (SCY)

We calculate your service credit years by dividing your total service credit months by 12. Twelve months equals one year of service credit. More about service credit.

Survivor

The individual you designate — when picking Options 2, 3 or 4 at retirement — to receive benefit payments after your death. This survivor options video provides a 2 minute overview of your benefits.

System/Plan

The retirement system and plan in which you are a member. DRS manages 7 systems and 3 plans. These combine to create a total of 15 different systems and plans. Your system is your area of public service. For example, PERS for Public Employees’ Retirement System or WSPRS for Washington State Patrol Retirement System. Your plan is the number attached to your system, Plan 1, 2 or 3.

TRS

Teachers’ Retirement System – One of the DRS retirement systems. See all plans.

Vested

The point at which you’ve earned a lifetime monthly pension (defined benefit).

- Plan 2: You are vested after earning five years of service credit.

- Plan 3: You are vested after earning 10 years of service credit, or after 5 years of service credit if at least 1 year was earned after age 44. There are no vesting requirements for the part of Plan 3 you fund (defined contribution) and you can take distributions at any time after you leave public employment.

Washington State Investment Board (WSIB)

This organization serves as a pension fund trustee, investing and accounting for trust fund dollars.

WSIB Investment Program

One of two investment program types available to Plan 3 members of PERS, SERS and TRS. If your investment contributions are in the WSIB fund, they are in the WSIB program. You can transfer funds between the two programs. The WSIB TAP fund is a monthly-valued fund, which means it can take 45-90 days to withdraw money from this fund.

WSPRS

Washington State Patrol Retirement System – One of the DRS retirement systems. See all plans.

Petitions and Appeals Glossary

Adjudicative proceeding – a hearing process described in the Administrative Procedure Act (Chapter 34.05 RCW)

Appeal – an administrative review of a DRS decision

Appellant – the person seeking administrative review in an appeal

Brief – written argument

Closing statement – a party’s statement made at the close of that party’s evidence that summarizes the evidence presented

Cross examination – a party’s questions of the other party’s witness

Direct examination – a party’s questions of their own witness

Final order – the Presiding Officer’s decision on an appeal

Exhibit – documentary evidence

Opening statement – a party’s statement made at the beginning of the hearing that describes the evidence to be presented and the theory of the party’s case

Presiding officer – the officer designated by DRS to hear and decide appeals

Pro se – an appellant not represented by legal counsel

RCW – Revised Code of Washington

Stipulation – an agreement parties reach about the facts

WAC – Washington Administrative Code