DRS Notice 25-013, New requirements coming for age 50+ catchup contributions

Applies to: DCP Employers

Subject: DRS Notice 25-013, New requirements coming for age 50+ catchup contributions

What’s changing?

Beginning Jan. 1, 2026, employers who offer Washington state’s Deferred Compensation Program (DCP) will be required to identify and report all highly compensated employees who are age 50 or older to DRS.

DCP age 50+ catch-up contributions for these employees will need to be reported as Roth. The change is being made because of the SECURE 2.0 Act Section 603. The change doesn’t apply to contributions made under the three-year catch-up provision.

What does highly compensated mean?

The term highly compensated is based on wages of the prior calendar year; it applies to employees who are age 50 or older and who in 2024 had $145,000 or more in FICA wages. This amount is subject to change each year by the IRS. We’ll share the official dollar amount after the IRS sends their report at the end of 2025.

Why are employers required to report this data to DRS?

The IRS requires the use of FICA wages to determine who is a highly compensated employee. DRS doesn’t have access to this data, because it’s maintained by employers. If an employee doesn’t have FICA wages, they are not required to be reported to DRS.

When will you need to provide data to DRS?

Reporting will be required in January of each year. We will send directions on how to report later.

For employers who rely on the Human Resource Management System (HRMS), this reporting will be done by the Office of Financial Management (OFM).

How this affects catch-up contributions for age 50+

For the employees you’ve identified as highly compensated, you’ll need to report DCP contributions above the regular IRS DCP limit as Roth.

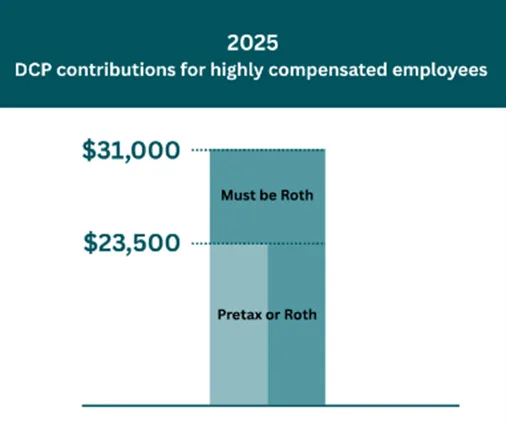

- You’ll receive a warning message when the participant is approaching the regular annual DCP limit. For 2025, the regular IRS limit is $23,500.

- Once the employee has contributed the regular annual limit, pretax contributions will no longer be accepted. All remaining contributions will need to be reported as Roth for the remainder of the calendar year.

- Example: If the person is paid once a month and evenly making pre-tax contributions to reach the 50+ max, their monthly contribution would be $2,583.33. At this rate, they would reach the IRS limit of $23,500 by September and all future contributions for the remainder of the year would need to be made as Roth.

Does the participant need to make a deferral change request to designate contributions as Roth once they have reached Mandatory Roth Contribution (MRC) status?

No, a participant who elects to make 50+ catch-up contributions is not required to make a deferral change to ensure catch-up contributions are reported as Roth. The employer should deduct and report 50+ catch-up contributions as Roth when required for highly compensated participants.

What is MRC status?

MRC stands for Mandatory Roth Contributions. When a participant is reported to DRS as highly compensated and have contributed the normal annual limit, they will be in MRC status. This will ensure that only Roth contributions are accepted for catch-up contributions.

About DCP catch-up contributions

Age 50+ catch-up contributions: Employees who are age 50 or older can contribute an additional $7,500 beyond the annual limit each year ($31,000 in 2025). These contributions are subject to MRC for highly compensated employees.

Three-year catch-up contributions: Employees can contribute up to twice the maximum ($47,000) during the three years before your normal retirement age. These contributions are not subject to MRC.

If you have any questions regarding this notice, contact Employer Support Services at 360-664-7200, option 2, or 800-547-6657, option 6 and then 2.