Chapter 11: Deferred Compensation

DCP overview

The Deferred Compensation Program (DCP) is an Internal Revenue Code (IRC) Section 457 program that provides an opportunity for employees to set aside dollars into a supplemental retirement account. In addition to pretax contributions, DCP also has a Roth option as of October 2023. The Roth option was enacted by the 2022 legislature. Deferred compensation is an agreement between employee and employer to postpone part of the employee’s income until separation from service. Once a member is automatically enrolled or joins DCP, they become a participant of the program.

Full-time state employees and employees of higher education are automatically enrolled when they’re hired unless they choose to opt out within 30 days from date they are officially notified about their enrollment. Default contributions are based on 3% of an employee’s pretax employment income. Employees who stay in DCP can change or suspend their contributions at any time.

Amounts deferred are held in trust by the Washington State Investment Board for the exclusive benefit of participants and their beneficiaries. Pretax deferrals reduce the taxable income reported on program participants’ Form W-2 for the calendar year it was deferred. Roth deferrals are taxed as income on the program participants’ Form W-2 for the calendar year it was deferred.

Any state employee (full time, part time, working a regular schedule or career seasonal) who hasn’t been automatically enrolled, including any elected or appointed official of the state, is eligible to participate in DCP at any time. Political subdivision employees may participate if DCP is offered as an employee benefit where they’re employed.

Local government employers may choose to participate in DCP automatic enrollment for their newly hired, full-time employees. To sign up for auto enrollment, local government employers must submit a signed resolution to DRS.

DCP is available to all state agencies and higher education institutions. Political subdivision and school district employers may add this program to their benefit package, provided their governing body adopts a resolution. See offering DCP.

Employer responsibilities

Reporting frequency and deadlines

Each payday, employers must submit a DCP transmittal report that reflects program participants’ deferral information.

For each payroll period, both the transmittal report and the payment must reconcile before the next report can be processed.

Transmittals not processed within five business days past the payroll date are late.

Both the transmittal report and the payment must be received and reconciled before the participant’s money can be invested.

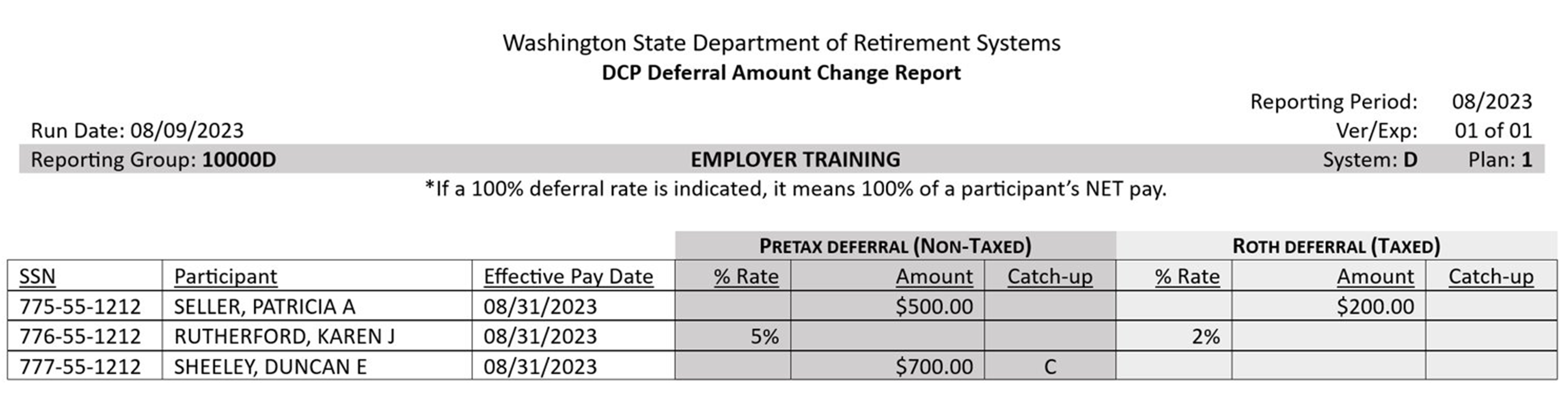

Deferral change report

The Deferral Change Report advises the employer of changes to DCP deductions. It is available to the employer three days before the cutoff date. The cutoff date is the number of days before payroll the employer sets as the cutoff for accepting changes. All employers will receive the DCP Deferral Change Report in ERA under Processes/My Documents.

Employers cannot start, stop, increase or decrease an employee’s deferral until the change appears on the DCP Deferral Change Report.

The DCP Deferral Change Report will reflect the following for both new and existing participants:

- The pay date when deferrals should begin

- Pretax and/or taxed (Roth) amount(s) elected by the employee

- A “C” indicator reference for three-year deferral catch ups

Employee enrollment

Auto-enrollment employers: you must report employee profile information and hire date to DRS by the end of the payroll cycle for newly-hired, full-time employees of state agencies and higher education (excluding student employees). This is referred to as automatic enrollment. See Chapter 8 for technical requirements.

Non-auto enrollment employers: employees not covered under automatic enrollment may enroll in DCP by completing a DCP Enrollment form available on the DCP website. When eligible to begin deferrals, the participant will be listed on the DCP Deferral Change Report sent to employers.

Annual limits for DCP Roth and pretax

The following limits apply to Roth and pretax deferrals. The combined deferrals for both options must fall within IRS annual limits.

2025 limits

In 2025, the maximum amount participants may defer from their annual compensation is $23,500.

Maximum Contribution: $23,500

Age 50 and Over Catch-up Contribution: additional $7,500

3-Year Catch-up Contribution: additional $23,500

At this time, DRS is not implementing the optional SECURE 2.0 Act provision that increases catch up contributions for individuals age 60 to 63.

Changing and suspending deferrals

Employees may change or stop their payroll deduction at any time by calling the DCP Information Line at 888-327-5596. Employees can also make changes by accessing their online accounts.

All deferral changes will be reported to employers on the Deferral Change Report for use in updating the payroll system. For employee leave of absence, deferrals can be temporarily suspended and restarted in the Member Management process in ERA.

Sample Deferral Change Report

Deferrals from lump sum payments

Participants can prearrange to defer a portion of a lump sum payment such as a cash out of unused annual leave or sick leave (if the employer participates in VEBA, sick leave may not be able to be deferred). The deferral must be arranged before the employee separates from employment; at least 30 days before separation is recommended.

Note: deferrals from severance payments are not allowed. Contact us if you have any questions about deferrals from other types of lump sum payments.

Participants can contact a DRS customer service representative at 360-664-7111 or contact us through their DRS online account to start the process.

When the deferral from the lump sum payment is requested by the participant, DRS will email the appropriate employer payroll contact with the following information:

- Name of participant

- Amount of lump sum

- Whether deferral is pretax or taxed (Roth) or a combination of both

- Date DRS expects the deferral

The deferral can be taken from the lump sum amount only, unless the participant requests their regular deferral as well.

If the lump sum payment will not be paid on the date indicated on the email from DRS, contact us at 360-664-7111 or email us.

Transmittal reporting

Employers may report through ERA Interactive, ERA Manual Upload or send files through secure file transfer (SFT). All employers will receive the Deferral Change Report electronically. See Chapter 8: Transmittal Reporting.

Employers are responsible for transmitting employee name or address changes to DRS on the transmittal as necessary. You don’t need to report changes on the retirement system transmittal report. Quarterly statements (DCP and Plan 3) for your employees are available in their online retirement accounts.

DCP End Dates

Report a DCP End Date on the DCP Report that includes the employee’s final DCP contribution. See Submit a separation date in an Interactive correction report or Submit a separation date in a regular Interactive transmittal report.

Submitting payments

State agencies

State Agency (HRMS) employers use an automated method of payment.

Political subdivisions and higher education

These employers may submit payments electronically or by check or warrant. See Chapter 10: Account Activity.

Form W-2 requirements

IRC Section 457 deferred compensation pretax deductions are reported on IRS Form W-2 at year end. Box 1 reduces ‘Wages, Tips, Other Compensation’ by the amount contributed to the Deferred Compensation Program. In box 12, enter a capital “G” and the amount the employee contributed to IRC Section 457.

Offering DCP

The smart, easy way to save

DCP is a supplemental retirement savings program offered by DRS to public employers at no cost. This benefit provides your employees with the opportunity to invest money through payroll deductions while offering options for federal tax savings.

Get started today!

To offer DCP to your employees, complete this resolution form and mail to DRS – we’ll handle the rest. Once you’ve adopted DCP, your employees can enroll with a few simple steps.

More than 1,000 employers are already participating in DCP. Here’s why:

A benefit for your employees

- Start saving with as little as 1% or $30 per month

- Low fees and portability

- Roth and pretax deferral options

- 24/7 account access

- No penalties for early withdrawals

- Responsive, friendly customer service

- Investing opportunities through WSIB

A benefit for employers

- All services are provided by DRS at no cost

- Simple reporting process

- DRS administers the plan

- Education provided by DRS

- Responsive, friendly employer support

- Helps with recruitment and retention

The DRS Education & Outreach Team is ready to assist you and your employees with this important decision. We provide education for state retirement plans and DCP. Whether you’d like to discuss the decision to adopt DCP or schedule a training event, call the Education & Outreach Team at 360-664-7005 – we’ll be glad to help.

Partnerships

DRS partners with the Washington State Investment Board (WSIB) and a third party record keeper to offer the Deferred Compensation Program. The goal is to help public employees save for their future while saving your organization time and money.

As one of the most successful public institutional investors in the country, WSIB selects and updates the investment options offered through DCP.

The DRS record keeper maintains the records for Plan 3, DCP and JRA customer investment accounts and assists customers with transactions related to these accounts.

DCP automatic enrollment

The Legislature enacted an automatic enrollment provision for the state’s Deferred Compensation Program (DCP). As of January 2017, state agencies and higher education employers are required to automatically enroll new full-time employees into DCP unless the employee opts out (Engrossed Substitute Senate Bill 5435).

Local governments offering DCP are not required to participate in automatic enrollment. However, they can elect to participate. Automatic enrollment can help employees save more for retirement. In similar efforts nationwide, 80-90% of auto-enrolled employees choose to stay in the savings plan.

Automatic enrollment FAQ

What are some important time frames?

- 30 days (30-day opt out period, or 30-day window) the amount of time a new employee has to opt out of DCP without having a deferral. The 30 days begin when the record keeper notifies the new hire about automatic enrollment.

- 90 days (90-day window, or permissible withdrawal period) the amount of time a new employee has to stop a deferral AND still withdraw any automatic enrollment contributions. The 90 days begin with the first deferral from an employee’s paycheck. At any time within the 90 days, if the employee makes an elective choice for their DCP account, the permissible withdrawal period ends.

What is considered “full-time?”

The definition of “full-time” for state agencies and institutions of higher education is defined in WAC 357-01-174. The definition of “full-time” for other public employers is at the organization’s discretion.

Are any full-time employees exempt from automatic enrollment?

Yes. Automatic enrollment does not include student employees, seasonal employees, or retirees returning to work, even if they fit the newly hired/full-time employee status.

How much will the employee contribute with automatic enrollment?

3% of pre-tax income is the default deferral rate. However, an employee may choose to defer a different percentage or set dollar amount at any time after the record keeper sets up their account.

When will employees be automatically enrolled?

When employers have a new hire, they will provide DRS with their information. DRS will pass this information to the record keeper who then sends communication to the new employee. The employee will have 30 days from the date of this communication to opt out of DCP.

When will employees make their first contribution?

Deferrals will begin after the 30-day opt out period or following any elective choice made by the employee. For those who default into DCP, their contributions will begin within a couple payroll periods following the 30-day window.

What is an “elective choice” under automatic enrollment?

If an employee selects an investment option or changes their deferral rate, this is considered an elective choice and it will impact their 30/90-day windows. If they are still in the 30-day opt out period, an elective choice will end the period and they will not have a 90-day permissible withdrawal period. If the election is made during the 90- day window, it will end the employee’s ability to request a permissible withdrawal unless they are setting their contribution amount to zero.

Will contributions be pretax or Roth?

Automatic enrollment DCP contributions are pretax.

Where will the contributions be invested?

If the employee does not make an investment selection, their contributions will be invested in the Retirement Strategy Fund that assumes they will retire at age 65.

How can the employee change their contribution amount or investments?

Employees can make these changes online or by phone. Log in to DCP through online account access or call 888-327-5596. Any elective change will cancel the employee’s rights to a permissible withdrawal* under the automatic enrollment rules.

What if the employee doesn’t want to be enrolled?

Newly hired employees can opt out online or by calling 888-327-5596.

If the employee opts out, can they join DCP at a later date?

Yes

Can the employee get their money back out of DCP if they choose to opt out following the first contribution?

Yes, this is known as the permissible withdrawal period. If the employee makes this choice within 90 days from first deferral date, they may withdraw their automatic enrollment contributions from DCP as long as the record keeper received the request within the 90 days.

How can the employee submit a permissible withdrawal request and is it still subject to tax withholding?

The employee can call the DCP record keeper at 888-327-5596 to request an auto enrollment withdrawal. The record keeper must receive the withdrawal request by the end of the 90-day window. Because the employee contributions are pretax dollars, the tax withholding is 10%.

Which employer groups are mandated to participate in automatic enrollment?

Employers who report through HRMS, 10 state commissions that don’t report through HRMS, the State Bar Association and higher education employers.

How will local employers sign up to participate in automatic enrollment?

To implement automatic DCP enrollment for your employees, complete this resolution form and mail to DRS.

If local employer elects into automatic enrollment, is it an irrevocable decision?

No. DRS will provide instructions if you choose to opt out in the future.

What are the reporting requirements for automatic enrollment?

If your organization chooses to participate in automatic enrollment, you will report the following employment information for new employees—separate from all other transmittal reporting. Provide the information once per newly hired employee and submit to DRS no later than the last day of the payroll cycle. This format must contain fixed length fields. Numeric data is unsigned and must be zero filled, i.e. July 1, 2016 = 20160701. Alpha data must be left justified and space filled. No contribution data should be sent for D1 until you receive notification the employee is enrolled in DCP.

| TRANSACTION-DATE | (N8) (Date Sent) |

|---|---|

| EMPLOYER-DCP-RPT-GRP | (A6) |

| SSN | (N9) |

| MBR-LAST-NAME | (A35) |

| MBR-FIRST-NAME | (A35) |

| MBR-MID-INITIAL | (A1) |

| ADDR1 | (A40) |

| ADDR1 | (A35) |

| CITY | (A30) |

| STATE | (A2) |

| ZIP-CODE | (A9) |

| GENDER-CODE | (A1) |

| BIRTH-DATE | (N8) |

| HIRE-DATE | (N8) |

Use the following naming convention for the new hire file: [anything.]autoenroll[.file extension] The “anything” section is at the discretion of the employer and could include reporting period The file name should contain no spaces and be no longer than 30 characters If the file is created in Excel, save it with the ‘.csv’ extension Place the new hire file on DRS’ secure file transfer (SFT) location for DRS retrieval.

DCP Employer resources

Contact information

360-664-7200

800-547-6657, option 6

dcpinfo@drs.wa.gov