Cost of Living Adjustment (COLA)

A cost-of-living adjustment (COLA) is an annual adjustment applied to retirement income to counteract cost changes in the economy (inflation). While most DRS retirement plans offer a COLA, Plan 1 members in PERS and TRS only have a COLA if they selected it during retirement.

If you’re in Plan 2 or 3 and have been retired at least one year, you’ll receive a cost-of-living adjustment (COLA) automatically each July — no matter how many years you worked.

2025 COLA changes

Most plan COLAs take effect July 1 and start with July 31 benefit payments.

The following table includes COLA percentages that apply to most DRS plans. This includes: PERS Plans 2 and 3, SERS Plans 2 and 3, TRS Plans 2 and 3, LEOFF Plan 2, WSPRS Plans 1 and 2 and PSERS Plan 2.

Will PERS 1 and TRS 1 receive a benefit increase this year?

No, legislation for the PERS 1 and TRS 1 increase did not pass. Those plans will not have an increase applied in 2025.

COLA percentages for most DRS plans (effective July 1, 2025)

| Retirement Dates | Adjustment |

|---|---|

| July 2, 2024 – July 1, 2025 | 0.00% |

| Prior to July 2, 2024 | 3.00% |

The JRS plan COLA for members who retired prior to June 30, 2013, is 3% (effective July 1, 2025).

COLA percentages for LEOFF Plan 1 (effective April 1, 2025)

| Retirement Dates | Adjustment |

|---|---|

| April 2, 2024 – March 31, 2025 | 0.00% |

| January 1, 2024 – April 1, 2024 | 3.61% |

| April 2, 2023 – December 31, 2023 | 9.33% |

| Prior to April 2, 2023 | 3.61% |

LEOFF Plan 1 COLAs are effective April 1 and included with April 30 benefit payments.

Historical COLA adjustments

Most plan COLA percentages are based on the Consumer Price Index (CPI) for the greater Seattle area. (The Judicial Retirement System bases its COLA on the CPI for U.S. cities.) COLA percentages are provided to us by Washington State law.

RCW 41.40.010 (15) through (18) defines the “index” that is used for measuring COLAs. The index is the annual average for the Consumer Price Index for the greater Seattle area. To view the annual average for the past several years, select the CPI-W graph near the bottom. These references are for PERS Plan 2, but other plans have similar descriptions.

This next information applies to customers in Plan 2, Plan 3, WSPRS Plan 1 and JRS. If you are a Plan 1 member in PERS, TRS or LEOFF, see the sections below for information specific to your plan COLA.

When will I receive a COLA?

You need to have been retired for at least one year by July 1. Once you are eligible, you will receive any COLA starting with the pension payment issued at the end of July, and every year after. You don’t need to apply to receive the COLA – it is automatic.

How much will the COLA be?

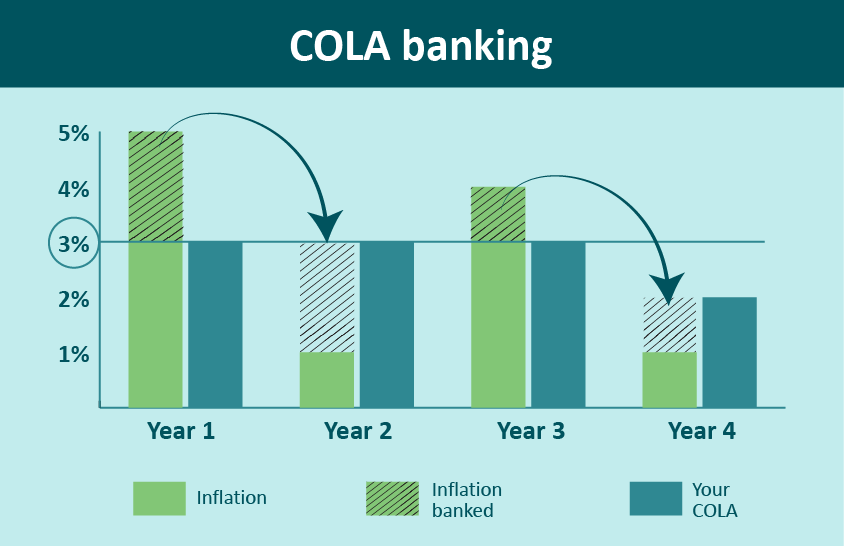

The maximum annual COLA you can receive for most DRS plans is 3%. If inflation that year is above 3%, the additional amount is applied to future adjustments (this is called COLA banking). Any year inflation is lower than 3%, the COLA can pull from banked percentages in prior years.

Most plan COLA percentages are based on the Consumer Price Index (CPI) for the greater Seattle area. (The Judicial Retirement System bases its COLA on the CPI for U.S. cities.) COLA percentages are provided to us by Washington State law.

RCW 41.40.010 (15) through (18) defines the “index” that is used for measuring COLAs. The index is the annual average for the Consumer Price Index for the greater Seattle area. To view the annual average for the past several years, select the CPI-W graph near the bottom. These references are for PERS Plan 2, but other plans have similar descriptions.

Example: How the COLA is calculated

Divide the annual index number from the prior year by the index number for the year prior to that. For the COLA applied in 2018, the index for 2017 is divided by the index for 2016. In looking at the chart that would be:

258.847/250.523= 1.033

This means that the calculated COLA is 3.3%. Since most plans have a COLA that is capped at 3%, the COLA applied in 2018 would be 3%, with the remaining .3% banked for a future year when the COLA is less than 3%. For instance, if the calculated 2019 COLA was 1.5%, the 0.3% overage from 2018 would be added to give a total COLA of 1.8% for 2019.

LEOFF 1 Plan does not have a cap on their COLA. In the example above, they would receive the full 3.3% COLA in 2018.

COLA banking

Most DRS plans have a feature called COLA banking. The maximum amount of growth the COLA has in any one year is 3%, however if inflation is over 3% in any year, the overage is banked, or applied, to any future year the inflation is below 3%. Most retirement plans with a cost of living adjustment either have a hard cap or no cap at all. COLA banking provides a form of smoothing for you, as well as the plan. For example, if inflation bounced between 6% and 0% for four years in a row (6, 0, 6, 0), your plan would still see a consistent 3% increase each year.

COLA banking happens automatically and your banked amounts can vary depending on how many years you’ve been retired from your plan as well as the inflation for those years. This variance means that even the same plan members may receive different COLAs some years, depending on the amount available in their COLA bank.

More about COLAs

LEOFF Plan 1 COLA

Eligibility: You need to have been retired for at least one year by April 1. Once you are eligible, you will receive any COLA starting with the pension check mailed out at the end of April, and every year after.

Maximum COLA: LEOFF Plan 1 Base COLA does not have a maximum and does not include COLA Banking. Based on your retirement date, you may qualify for a first-year COLA adjustment.

PERS and TRS Plan 1 COLA

Optional COLA: PERS and TRS Plan 1 members have an optional COLA they can request when applying for retirement. Eligible members can choose to reduce their initial retirement income in exchange for an annual automatic cost of living adjustment. The Optional COLA has no age requirement and is limited to a maximum of 3% of your monthly benefit. The Consumer Price Index for the greater Seattle (CPI-W) is used to calculate the Optional COLA.

To compare your benefit with and without the Optional COLA, try the Optional COLA Calculator.

Other PERS and TRS Plan 1 COLA provisions

Adjusted Minimum Benefit: Qualifying PERS and TRS Plan 1 members receive an automatic annual adjusted minimum benefit if they:

- Have at least 25 years of service credit and have been retired at least 20 years;

or - Have at least 20 years of service credit and have been retired at least 25 years.

You also must have a monthly pension below the current minimum benefit amount to qualify for this increase. For example, in 2022 the minimum amount was $2,138.

Age 65 COLA: Only retirees who chose this COLA in 1995 are eligible.